How 14 Days of Investor-Grade Market Research Helped a HealthTech Startup Walk Into a ₹12Cr Series A Knowing Their Market Better Than Their Investor Did.

PART 1 — THE SITUATION

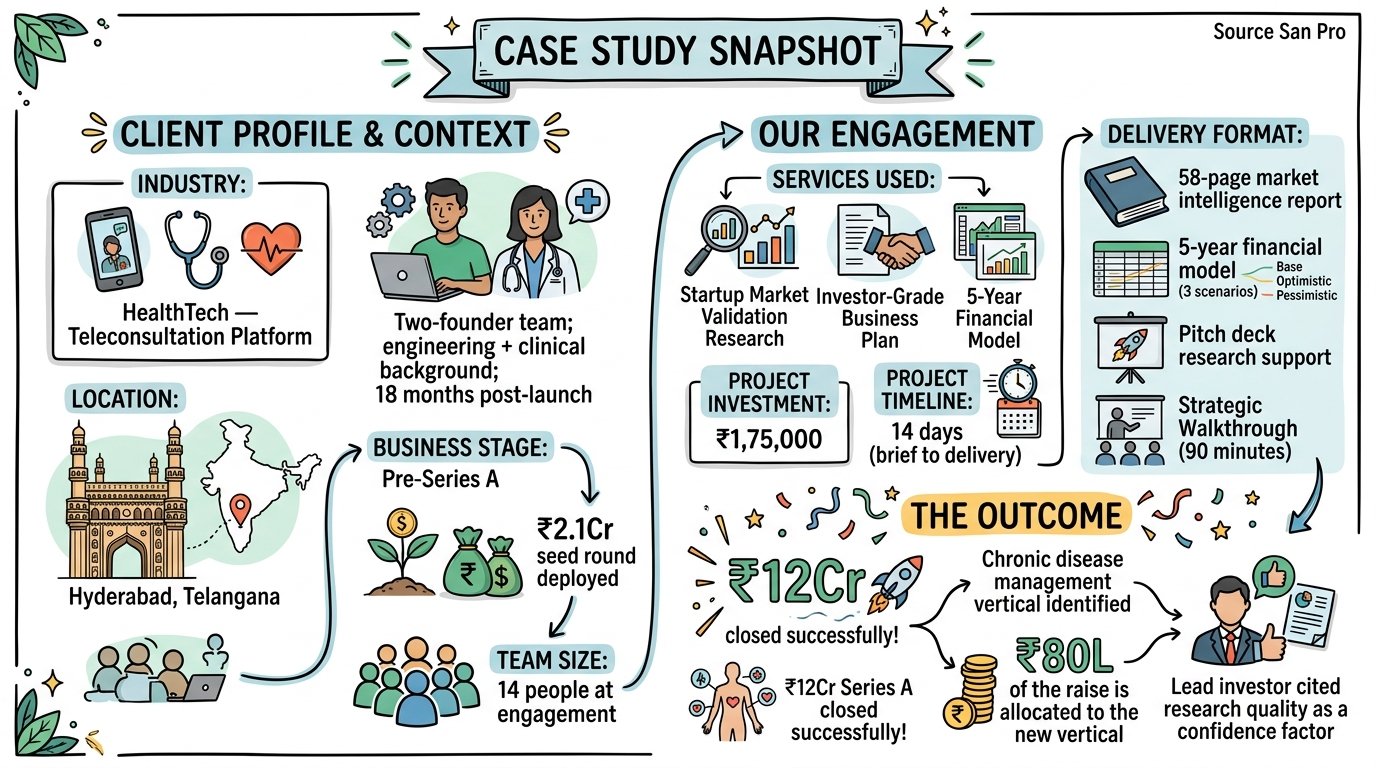

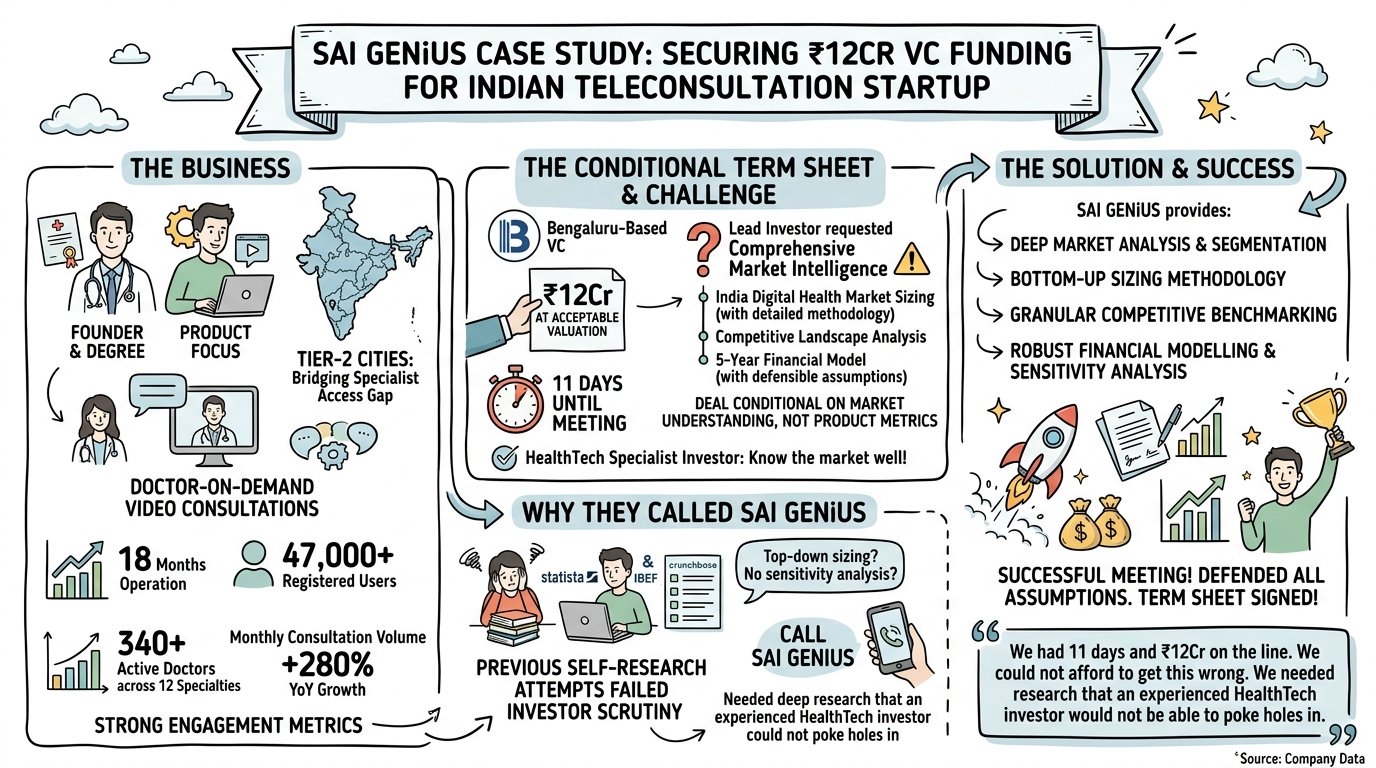

The business: Two founders — one with a clinical medicine background, one with engineering and product experience — had built a teleconsultation platform specifically designed for India’s Tier-2 cities: doctor-on-demand video consultations for patients in cities where specialist access required 60–120 minute travel to the nearest tier-1 hospital. After 18 months of operation, the platform had 47,000 registered users, 340 active doctors across 12 specialties, and a monthly consultation volume that had grown 280% year-over-year.

The product worked. The engagement metrics were strong. The founders had received a term sheet from a Bengaluru-based VC — one they had been in conversation with for six months — for ₹12Cr at a pre-money valuation they found acceptable.

The problem: The term sheet was conditional. Before signing, the lead investor had requested comprehensive market intelligence: India digital health market sizing (with methodology), competitive landscape analysis, and a 5-year financial model with defensible assumptions. The investor had been explicit: the deal would proceed on market understanding, not product metrics alone.

The investor meeting — the one that would determine whether the term sheet converted to a signed agreement — was 11 days away.

Why they called SAI GENiUS: The founders had previously tried to produce market research themselves. They had assembled a market sizing document from publicly available Statista and IBEF reports, a competitor list from Crunchbase, and financial projections built from first-principles unit economics. The investor had looked at their materials in a previous meeting and politely noted that the market sizing methodology was top-down and the financial model lacked sensitivity analysis.

They needed something that would hold up under interrogation by an investor who, as a HealthTech specialist, knew the market better than most.

“We had 11 days and ₹12Cr on the line. We could not afford to get this wrong. We needed research that an experienced HealthTech investor would not be able to poke holes in.”

PART 2 — THE RESEARCH BRIEF

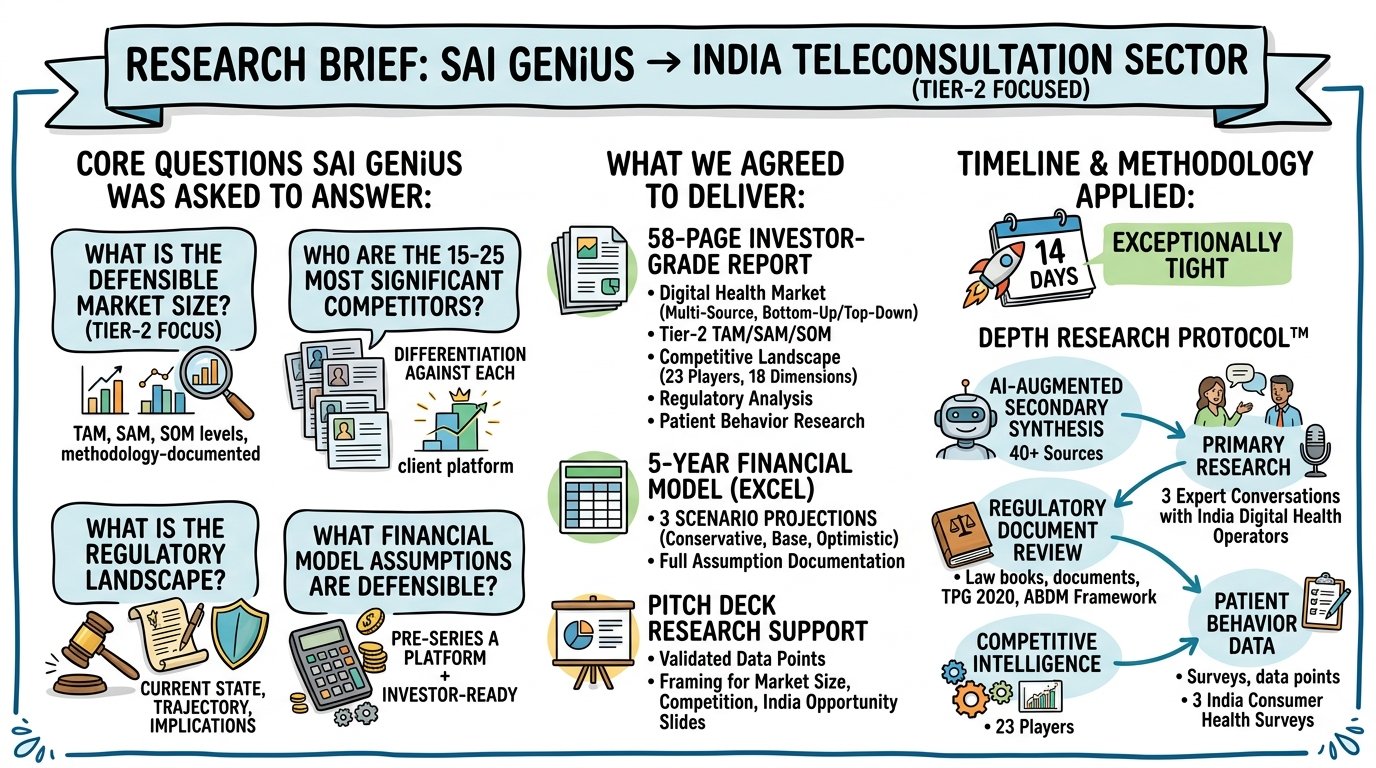

The core questions SAI GENiUS was asked to answer:

What is the defensible, methodology-documented market size for India’s teleconsultation sector — specifically Tier-2 focused — at TAM, SAM, and SOM levels?

Who are the 15–25 most significant competitors in the Indian teleconsultation space, and how does this client’s platform specifically differentiate against each?

What is the regulatory landscape for teleconsultation in India — current state, trajectory, and implications for the business model?

What financial model assumptions are defensible for a pre-Series A teleconsultation platform — for an investor who will challenge every line?

What we agreed to deliver:

58-page investor-grade market intelligence report covering: India digital health market (with multi-source, bottom-up and top-down verified sizing methodology), Tier-2 teleconsultation TAM/SAM/SOM, competitive landscape (23 players across 18 dimensions), regulatory analysis, and patient behavior research

5-year financial model in Excel with three scenario projections (conservative, base, optimistic) and full assumption documentation

Pitch deck research support: validated data points and framing for the market size, competitive landscape, and India opportunity slides

Timeline: 14 days — exceptionally tight for a 58-page investor-grade document

Methodology applied: DEPTH Research Protocol™ — AI-augmented secondary synthesis across 40+ sources; primary research including 3 expert conversations with India digital health sector operators; regulatory document review (Telemedicine Practice Guidelines 2020, ABDM framework documents); competitive intelligence across 23 players; patient behavior data from three India consumer health surveys (publicly available, methodology-documented)

PART 3 — WHAT THE RESEARCH FOUND

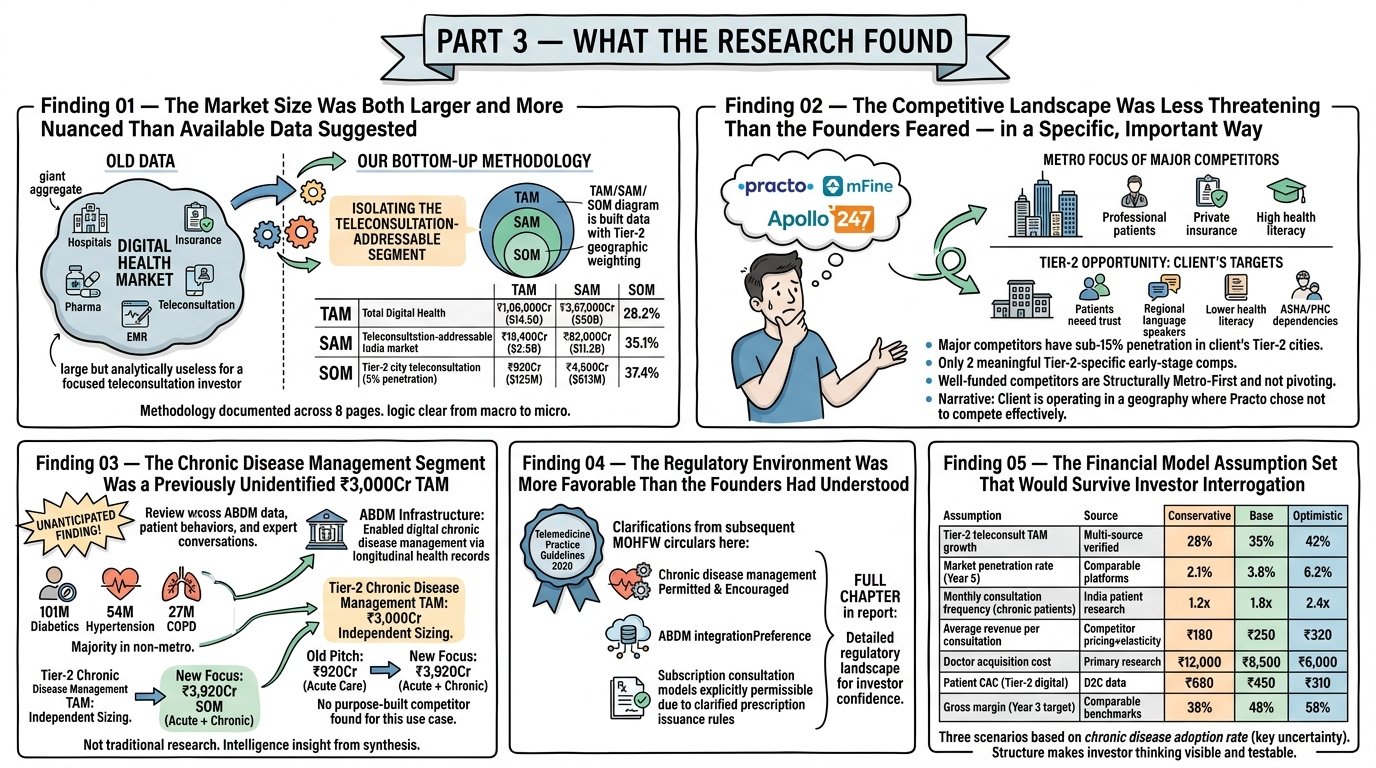

Finding 01 — The Market Size Was Both Larger and More Nuanced Than Available Data Suggested

Most available India digital health market reports cited aggregate numbers that included hospital management software, electronic medical records, health insurance technology, pharmaceutical e-commerce, and teleconsultation in a single figure, making the number large but analytically useless for a focused teleconsultation investor.

Our bottom-up methodology broke the market into its parts, isolated the teleconsultation-addressable segment, and built a TAM/SAM/SOM specific to the Indian teleconsultation opportunity with Tier-2 geographic weighting:

Market Level

Definition

2024 Value

2029 Projection

CAGR

TAM

Total India digital health market

₹1,06,000Cr ($14.5B)

₹3,67,000Cr ($50B)

28.2%

SAM

Teleconsultation-addressable India market

₹18,400Cr ($2.5B)

₹82,000Cr ($11.2B)

35.1%

SOM

Tier-2 city teleconsultation (5% penetration)

₹920Cr ($125M)

₹4,500Cr ($613M)

37.4%

The methodology documentation occupied 8 pages of the report — not because length creates credibility, but because every assumption had a source, and every source was cited, and the investor could follow the logic from macro data to micro market opportunity without taking anything on faith.

Finding 02 — The Competitive Landscape Was Less Threatening Than the Founders Feared — in a Specific, Important Way

The founders believed they were competing directly with Practo, mFine, and Apollo 247 — three well-funded, nationally scaled teleconsultation platforms. The competitive landscape analysis revealed something more nuanced:

All three of these platforms had significantly concentrated their resources in metro markets. Their doctor networks, their marketing spend, their referral partnerships, and their product features were oriented toward metro patients — urban professionals with private insurance, high health literacy, and comfort with digital interfaces.

The Tier-2 patient profile — lower health literacy, higher trust requirement, preference for regional language consultation, ASHA and PHC relationship dependency — was being poorly served by metro-optimized platforms. All three major competitors had sub-15% penetration in the client’s target Tier-2 cities.

The more significant finding: across 23 competitors mapped, only 2 had any meaningful Tier-2 specific product development. Both were very early-stage with limited funding. The well-funded competitors were structurally metro-first — and showed no evidence of imminent Tier-2 pivot.

The competitive positioning that emerged: The client was not competing with Practo. They were operating in a geography where Practo had chosen not to compete effectively. This is a fundamentally different competitive narrative — and a significantly more fundable one.

Finding 03 — The Chronic Disease Management Segment Was a Previously Unidentified ₹3,000Cr TAM

This was the finding that neither the founders nor we had anticipated at the start of the research.

During our review of ABDM (Ayushman Bharat Digital Mission) documentation, patient behavior data, and expert conversations, a secondary market opportunity emerged that the founders had not considered in their original product scope: chronic disease management for Tier-2 patients.

India has 101 million diabetics (the largest diabetic population in the world), 54 million hypertension patients, and 27 million COPD patients — the vast majority in non-metro markets where consistent specialist follow-up is logistically impossible through traditional healthcare channels. ABDM’s longitudinal health record infrastructure was specifically designed to enable digital chronic disease management — a use case that required exactly the kind of trusted, repeated, Tier-2-accessible teleconsultation infrastructure the client had built.

The chronic disease management TAM for Tier-2 India — patients requiring minimum monthly specialist follow-up consultations, able to pay ₹200–₹400 per consultation — was independently sized at approximately ₹3,000Cr. No existing teleconsultation player had purpose-built a chronic disease management protocol. The regulatory environment (ABDM integration, telemedicine guidelines) was specifically favorable for this use case.

The implication: The pitch the founders had been making — acute care teleconsultation for Tier-2 patients — was a ₹920Cr SOM opportunity with competition from well-funded metro players approaching Tier-2. The pivot to include chronic disease management as a primary use case — not just acute care — was a ₹3,920Cr combined SOM opportunity with no purpose-built competitor.

This was not a research finding in the traditional sense. It was an intelligence insight that emerged from connecting regulatory infrastructure data, patient behavior data, and competitive white-space analysis — the kind of synthesis that requires both AI-powered source aggregation and human strategic interpretation to produce.

Finding 04 — The Regulatory Environment Was More Favorable Than the Founders Had Understood

The Telemedicine Practice Guidelines 2020 — India’s primary regulatory framework for teleconsultation — had been expanded and clarified in subsequent MOHFW circulars in ways that most operators in the space had not fully tracked. Specifically:

Chronic disease management via teleconsultation was explicitly permitted and encouraged under the current regulatory framework

ABDM integration created a regulatory preference for platforms that connected to the digital health records infrastructure — something the client’s technology was positioned to do with 6 months of development

Prescription issuance rules for chronic conditions had been clarified in ways that made subscription-based consultation models (a higher-LTV model than per-consultation) explicitly permissible.

The regulatory analysis occupied a full chapter of the report — because an investor who has been burned by regulatory risk in HealthTech needs to understand the specific regulatory landscape in detail, not just the headline “this sector is permitted.”

Finding 05 — The Financial Model Assumption Set That Would Survive Investor Interrogation

The 5-year financial model was built from verified, sourced market assumptions — not founder estimates. Every key driver was documented:

Assumption

Source

Conservative

Base

Optimistic

Tier-2 teleconsultation TAM growth

Multi-source verified

28% CAGR

35% CAGR

42% CAGR

Market penetration rate (Year 5)

Comparable platforms

2.1%

3.8%

6.2%

Monthly consultation frequency (chronic patients)

India patient behavior research

1.2x/month

1.8x/month

2.4x/month

Average revenue per consultation

Competitor pricing + elasticity research

₹180

₹250

₹320

Doctor acquisition cost

Primary research

₹12,000

₹8,500

₹6,000

Patient CAC (Tier-2 digital)

D2C health benchmark data

₹680

₹450

₹310

Gross margin (Year 3 target)

Comparable platform benchmarks

38%

48%

58%

The model’s three scenarios were not optimistic/realistic/pessimistic in the traditional sense — they were three different market penetration trajectories based on the chronic disease management adoption rate, which was the key uncertainty variable in the model. An investor could disagree with the chronic disease adoption assumption and immediately see what that disagreement implies for the 5-year financial outcome.

This is what sophisticated investor modeling looks like: not a number, but a structure that makes the investor’s own thinking visible and testable.

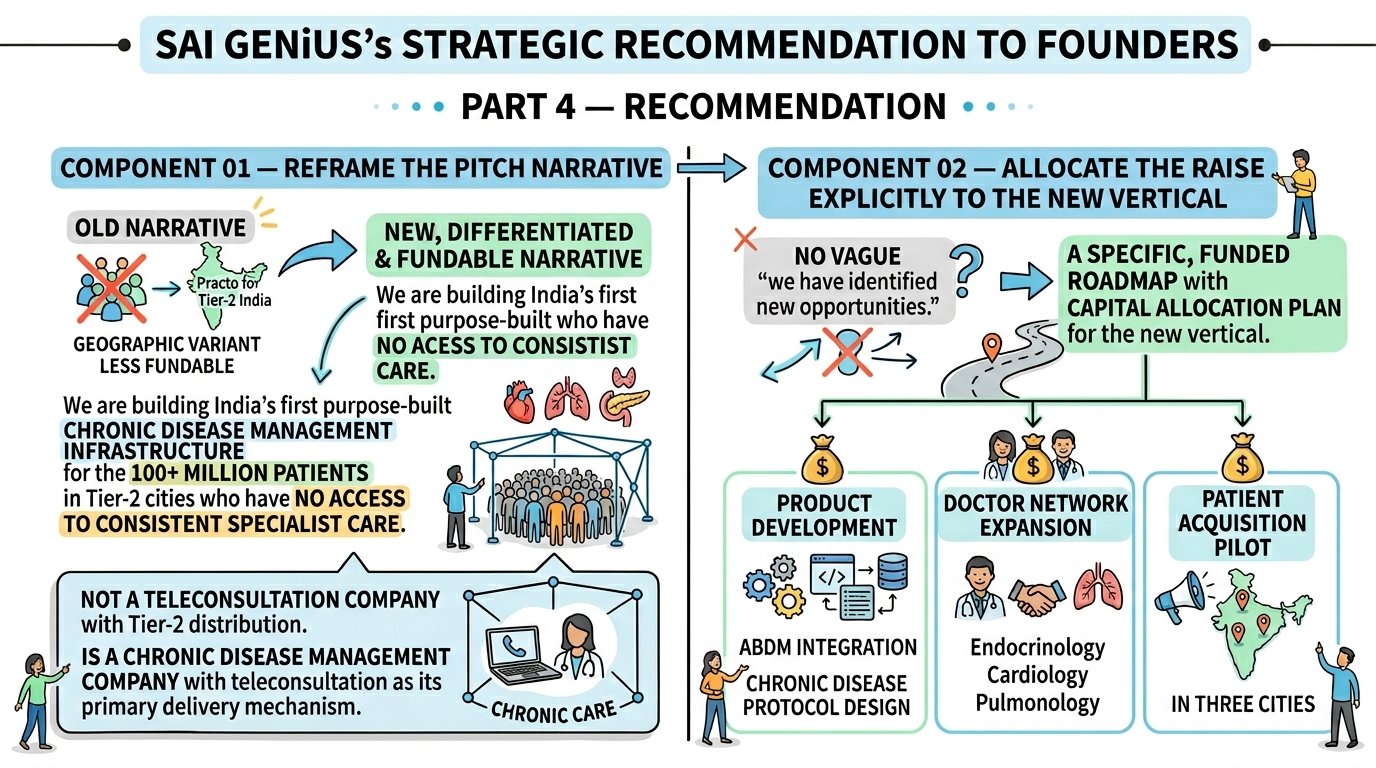

PART 4 — THE RECOMMENDATION

SAI GENiUS’s strategic recommendation to the founders had two components:

Component 01 — Reframe the pitch narrative. The pitch narrative the founders had been using — “we are building the Practo for Tier-2 India” — positioned them as a geographic variant of an existing product. The research supported a more differentiated and more fundable narrative: “We are building India’s first purpose-built chronic disease management infrastructure for the 100+ million patients in Tier-2 cities who have no access to consistent specialist care.” This was not a teleconsultation company with Tier-2 distribution. It was a chronic disease management company with teleconsultation as its primary delivery mechanism.

Component 02 — Allocate the raise explicitly to the new vertical The research had identified the chronic disease management opportunity with enough specificity that the founders could walk into the investor meeting with a capital allocation plan for the new vertical — product development (ABDM integration, chronic disease protocol design), doctor network expansion in relevant specialties (endocrinology, cardiology, pulmonology), and a patient acquisition pilot in three cities. This was not a vague “we have identified new opportunities.” It was a specific, funded roadmap.

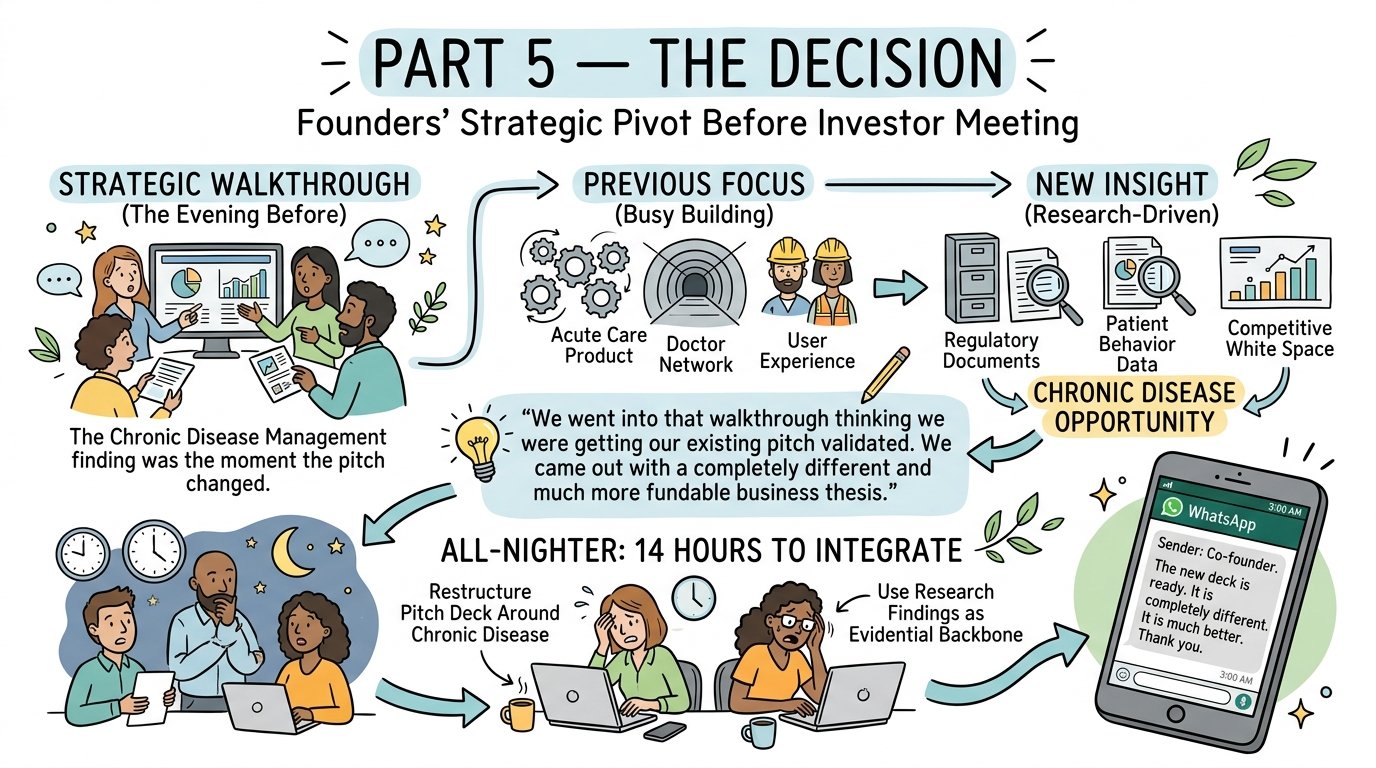

PART 5 — THE DECISION

The founders reviewed the research at the Strategic Walkthrough — a 90-minute session the evening before their investor meeting.

The chronic disease management finding was the moment the pitch changed. The founders had not seen this opportunity in 18 months of building in the space — not because they were not smart or observant, but because they had been building, not researching. Their attention was on the acute care product, the doctor network, and the user experience. The regulatory documents, the patient behavior data, and the competitive white space that together surfaced the chronic disease opportunity were simply not in their daily information environment.

“We went into that walkthrough thinking we were getting our existing pitch validated. We came out with a completely different and much more fundable business thesis. We had 14 hours to integrate it before the meeting.”

The founders worked through the night to restructure their pitch deck around the chronic disease management opportunity, using the research findings as the evidential backbone of the new narrative. At 3:00 AM, the co-founder sent us a WhatsApp message: “The new deck is ready. It is completely different. It is much better. Thank you.”

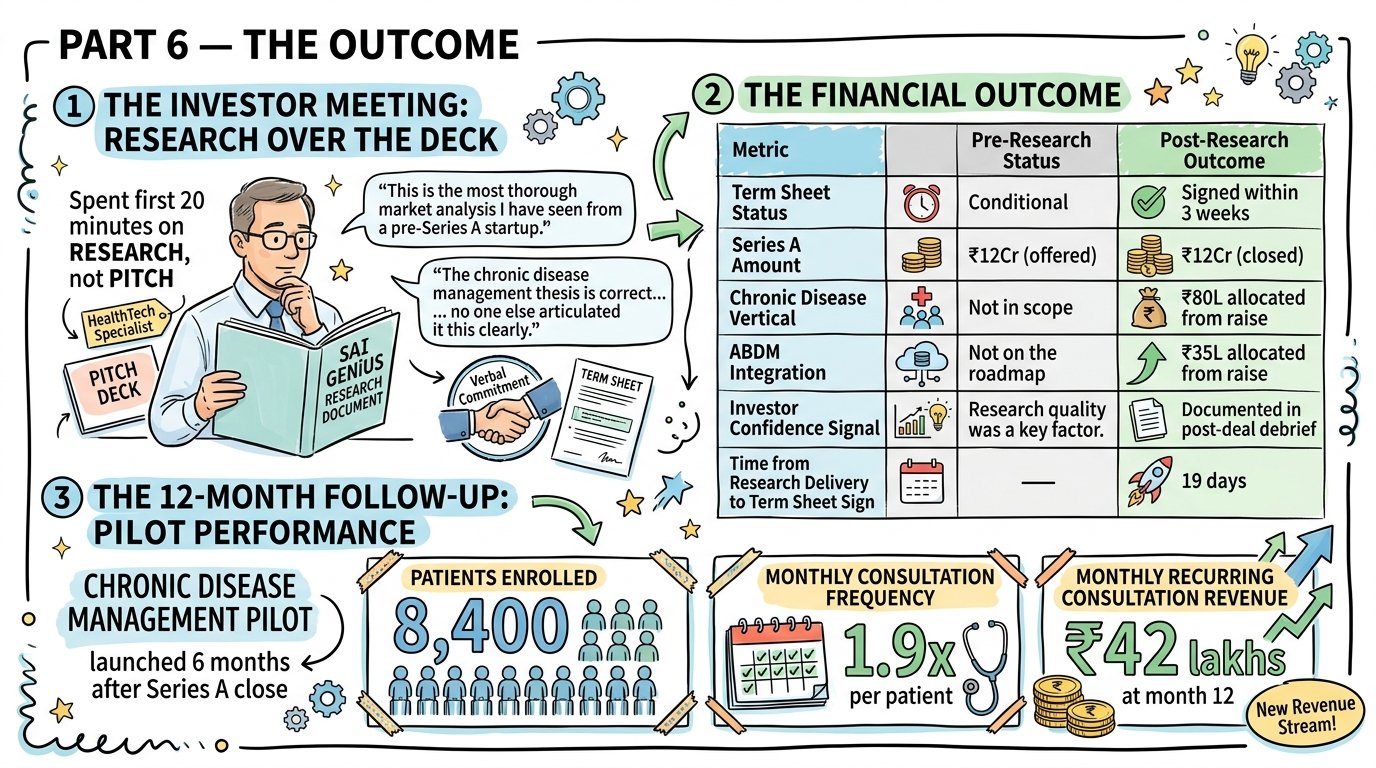

PART 6 — THE OUTCOME

The investor meeting: The lead investor — a HealthTech specialist who had reviewed over 200 India digital health decks — spent the first 20 minutes of the meeting examining the SAI GENiUS research document, not the pitch deck. According to the founders, he said: “This is the most thorough market analysis I have seen from a pre-Series A startup. The chronic disease management thesis is correct, and I am surprised no one else has articulated it this clearly.”

The meeting ended with a verbal commitment to proceed to a term sheet on the updated thesis.

The financial outcome:

Metric

Pre-Research Status

Post-Research Outcome

Term Sheet Status

Conditional

Signed within 3 weeks

Series A Amount

₹12Cr (offered)

₹12Cr (closed)

Chronic Disease Vertical

Not in scope

₹80L allocated from raise

ABDM Integration

Not on the roadmap

₹35L allocated from raise

Investor Confidence Signal

“Research quality was a key factor.”

Documented in post-deal debrief

Time from Research Delivery to Term Sheet Sign

—

19 days

The 12-month follow-up: The chronic disease management pilot — launched 6 months after the Series A close — had enrolled 8,400 patients by month 12 with a monthly consultation frequency of 1.9x per patient. Monthly recurring consultation revenue from the chronic disease vertical was ₹42 lakhs at month 12 — a revenue stream that did not exist before the research engagement identified the opportunity.

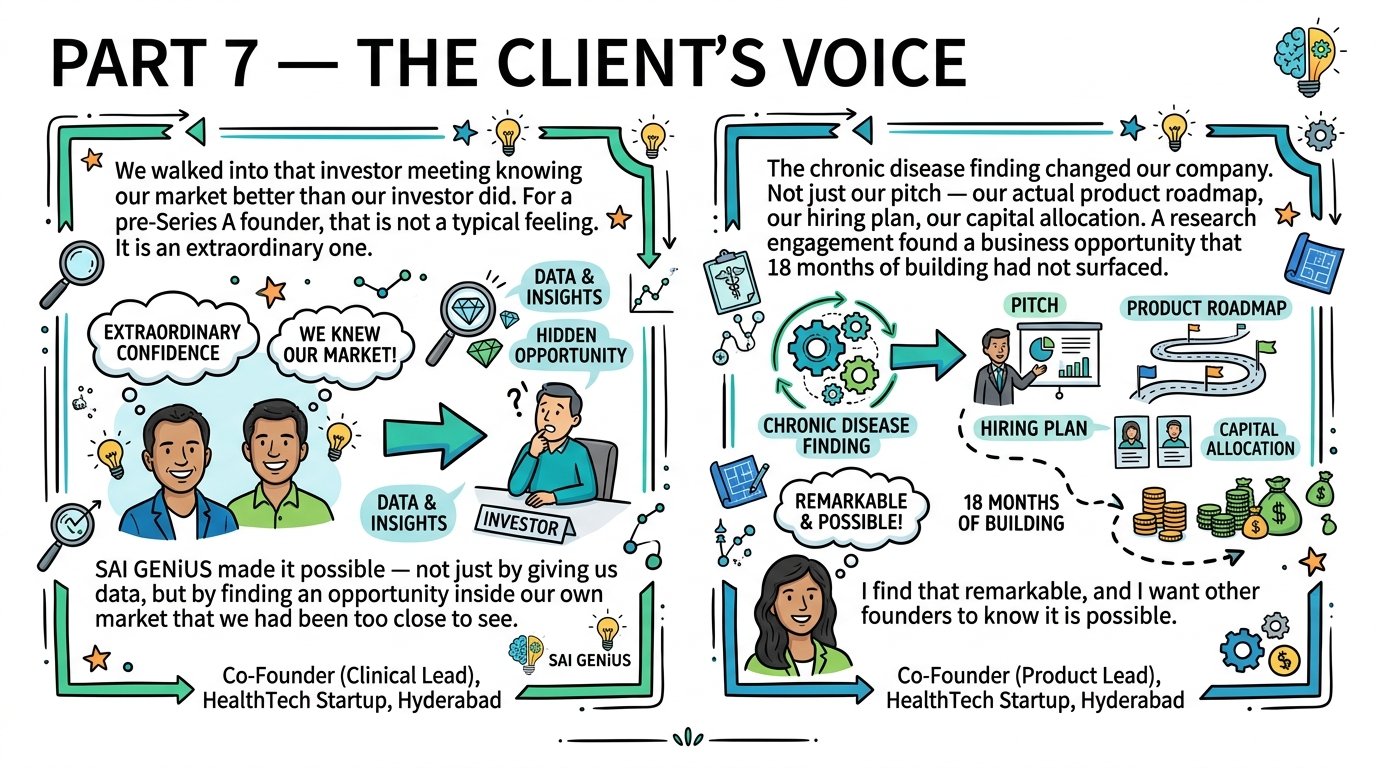

PART 7 — THE CLIENT’S VOICE

“We walked into that investor meeting knowing our market better than our investor did. For a pre-Series A founder, that is not a typical feeling. It is an extraordinary one. SAI GENiUS made it possible — not just by giving us data, but by finding an opportunity inside our own market that we had been too close to see.” — Co-Founder (Clinical Lead), HealthTech Startup, Hyderabad

“The chronic disease finding changed our company. Not just our pitch — our actual product roadmap, our hiring plan, our capital allocation. A research engagement found a business opportunity that 18 months of building had not surfaced. I find that remarkable, and I want other founders to know it is possible.” — Co-Founder (Product Lead), HealthTech Startup, Hyderabad.

PART 8 — THE CROSS-SECTOR LESSON

What this case study teaches any Indian founder approaching a fundraiser:

Lesson 01: The strongest fundraising narratives are built from market intelligence, not product metrics. Every founder has product metrics. The ones who walk in knowing their competitive white-space, their regulatory environment, and their TAM methodology in depth are the ones who convert investor conversations into signed term sheets.

Lesson 02: You cannot see your own market when you are inside its building. The chronic disease management opportunity had been hiding in plain sight — in regulatory documents the founders had read, in patient behavior data that existed publicly, in a competitivewhite spacee that their own product was uniquely positioned to fill. Seeing it required someone outside the building who was looking for it systematically.

Lesson 03: Investor-grade research is not about length — it is about methodology documentation. The reason sophisticated investors respect independent research is not the page count. It is the ability to trace every significant claim back to a verifiable source. Methodology documentation is the difference between research that holds up under scrutiny and research that collapses on the first challenging question.

Lesson 04: Research commissioned before a fundraiser does not just support the raise — it can change the company. The ₹3,000Cr chronic disease management opportunity was not a fundraise narrative enhancement. It was a product and business strategy discovery that is now generating ₹42 lakhs per month in recurring revenue. The research paid for itself before the term sheet was signed.

At vero eos et accusamus et iusto odio digni goikussimos ducimus qui to bonfo blanditiis praese. Ntium voluum deleniti atque.