CASE STUDY — Regional FMCG Distributor | Competitive Benchmarking + Monthly Retainer | Ahmedabad

CASE STUDY

FMCG Distribution (Regional Distributor — Gujarat)

Ahmedabad, Gujarat

Established SME (₹22Cr annual revenue; operating for 19 years)

Competitive Benchmarking Report + Supplier Market Mapping + Monthly Intelligence Retainer

₹80,000 (initial research) + ₹28,000/month (retainer, ongoing)

9 days (initial research)

Portfolio reallocation strategy — reduction of national FMCG brand dependence; addition of 3 premium regional brand partnerships

Gross margin +18 percentage points; revenue ₹22Cr → ₹26.4Cr in 12 months; 3 new premium brand contracts secured

~54x (₹4.4Cr revenue uplift + margin improvement value / ₹80,000 research investment)

CLIENT VOICE

"I had been in this business for 19 years, and I thought the margin compression was just the market. It turns out three of my direct competitors had already solved the problem by doing something I could have done at any point in the last three years. The research did not give me an exotic strategic insight. It showed me what was happening in my own city, in businesses just like mine, that I had not been paying attention to. The premium brand pipeline finding was the most immediately actionable piece of market intelligence I have ever received. I signed the first authorization agreement six days after reading the report."

— Managing Partner, Regional FMCG Distribution Business, Ahmedabad (Identity anonymized with permission)

Nineteen Years of Business, Two Years of Margin Collapse, and a Problem With No Visible Solution

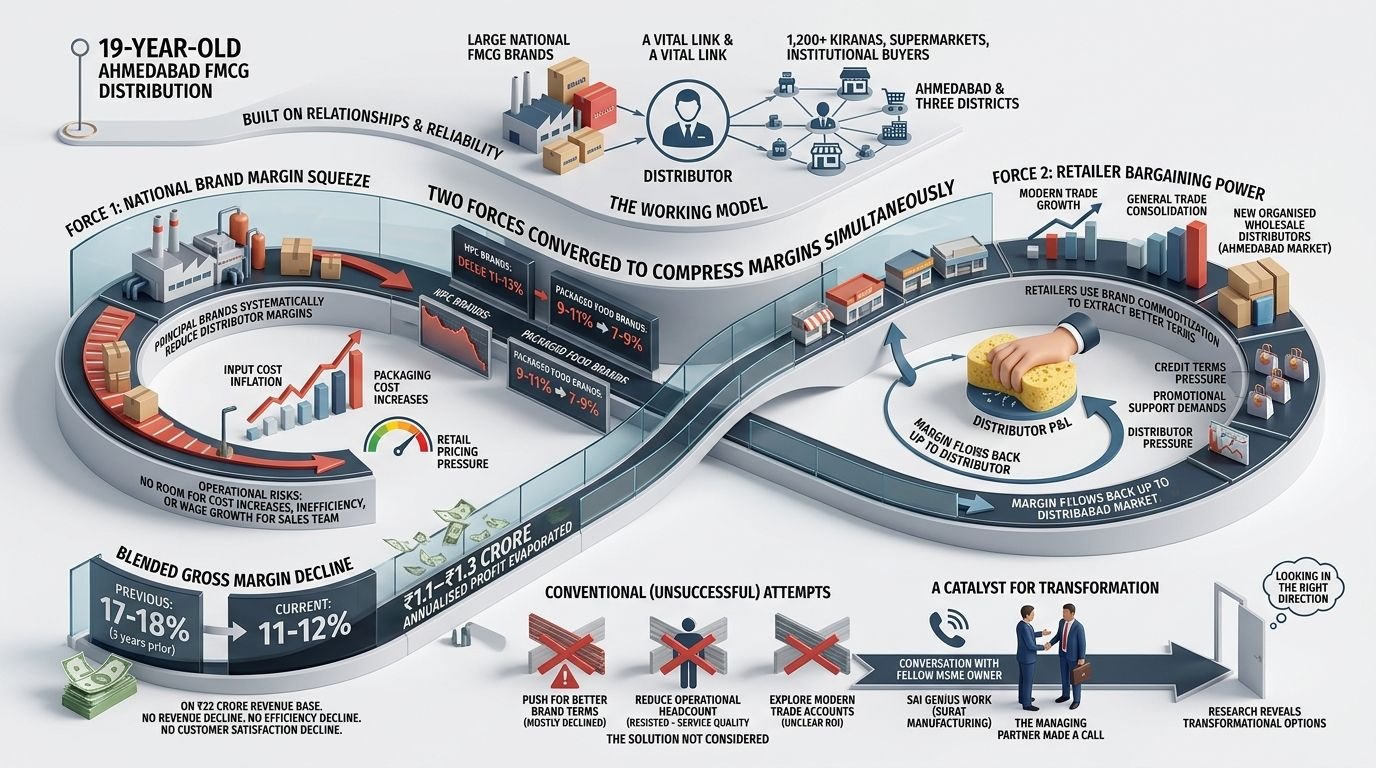

The managing partner of a 19-year-old Ahmedabad FMCG distribution business had built his company the way most successful regional distributors build theirs: through relationships, reliability, and the slow accumulation of principal brand authorisations across packaged food, household care, and personal care categories. At its core, the business operated as a critical logistics and retail access intermediary between large national FMCG brands and the 1,200+ kiranas, supermarkets, and institutional buyers it served across Ahmedabad and three surrounding districts.

The business model had worked for nearly two decades. Until it started not working.

Two forces had converged over the preceding three years to compress the margins of every national FMCG brand in the managing partner's portfolio simultaneously:

National brand margin squeeze: Every major national FMCG principal had systematically reduced distributor margins over 3 years as input cost inflation, packaging cost increases, and retail pricing pressure were progressively absorbed by the distribution layer. Distributor margins on HPC (home and personal care) national brands had declined from 11–13% to 8–10% across the portfolio. On packaged food brands, the decline was from 9–11% to 7–9%. The new margin levels were not loss-making, but they left virtually no room for operational cost increases, working capital inefficiency, or the wage growth required to retain the experienced field sales team the business depended on.

Retailer bargaining power: The parallel growth of modern trade, general trade consolidation, and the arrival of three organised FMCG wholesale distributors in the Ahmedabad market had increased retailer bargaining power in a way that had been invisible during the business's decade of growth. Retailers who previously accepted whatever margin the distributor offered were now comparing across 3–4 competing distributors before placing orders for national brands, using the commoditization of those brands to extract better credit terms and promotional support. Each percentage point of margin compressed at the retail end flowed directly back up to the distributor's P&L.

The managing partner's blended gross margin had declined from 17–18% (three years prior) to 11–12% (current). On a ₹22 crore annual revenue base, this margin compression represented approximately ₹1.1–₹1.3 crore in annualised profit that had effectively evaporated — without any decline in revenue, operational efficiency, or customer satisfaction.

His attempts to address the problem had been conventional: push for better terms from principal brands (mostly declined), reduce operational headcount (resisted because of the service quality implications), and explore whether modern trade account wins could offset general trade margin compression (unclear ROI).

The solution he had not considered: change the composition of the brand portfolio itself.

A conversation with a fellow MSME owner at a local business association meeting mentioned SAI GENiUS work with a manufacturing business in Surat. The managing partner made a call. He did not expect the research to reveal anything transformative; he thought he knew his market, his competitors, and his options. He was partially right. He had not looked in the right direction.

Three Findings That Reframed the Entire Business Model

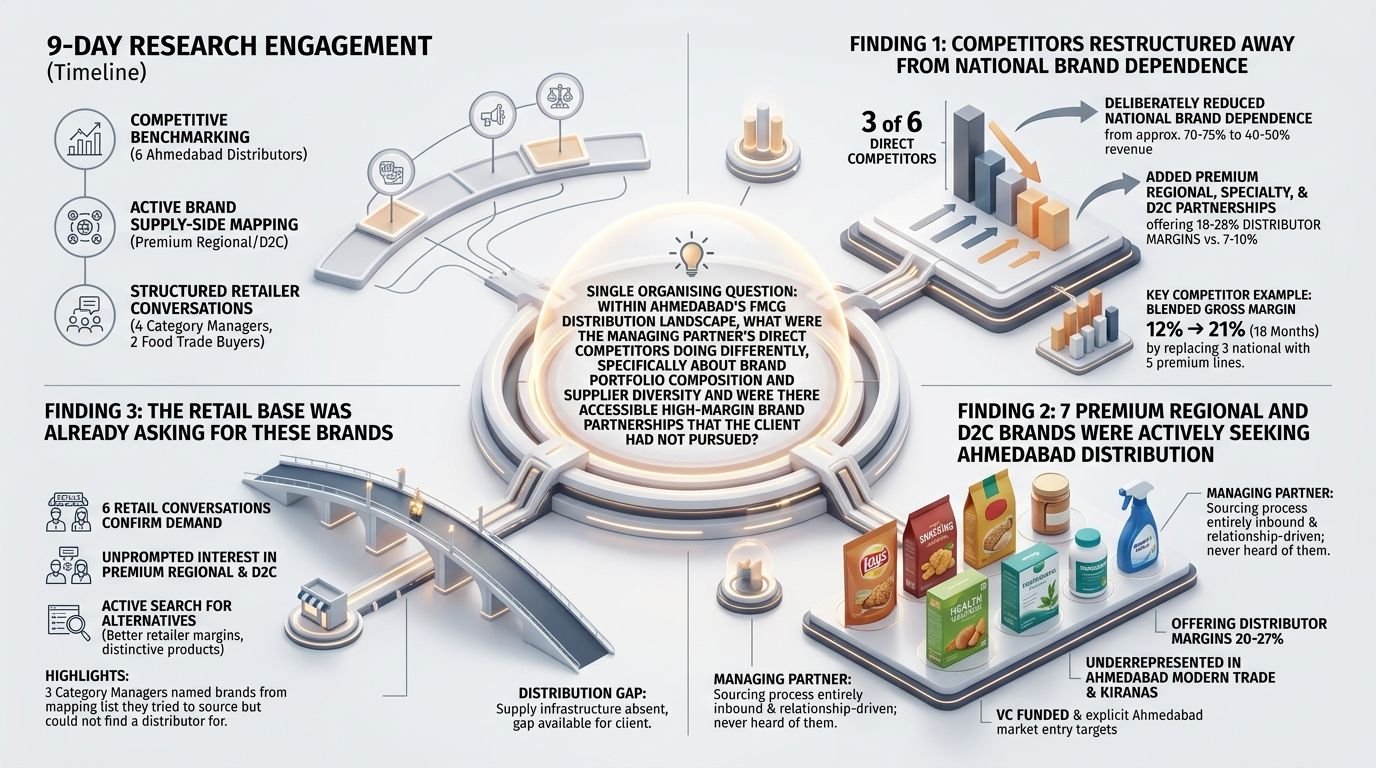

The SAI GENiUS research engagement was structured around a single organising question: within Ahmedabad's FMCG distribution landscape, what were the managing partner's direct competitors doing differently, specifically about brand portfolio composition and supplier diversity and were there accessible high-margin brand partnerships that the client had not pursued?

The 9-day research combined competitive benchmarking (direct analysis of 6 comparable Ahmedabad-based FMCG distributors, using trade association data, retail channel conversations, and distributor-level public and semi-public information) with an active brand supply-side mapping (identification of premium regional and D2C FMCG brands seeking Ahmedabad distribution and the margin structures they were offering).

The research team also conducted structured conversations with 4 Ahmedabad retail category managers and 2 organised food trade buyers, specifically to understand their evolving brand sourcing preferences and willingness to range premium and regional brands alongside national incumbents.

Three Direct Competitors Had Already Quietly Restructured Away from National Brand Dependence

The competitive benchmarking produced a finding that was simultaneously obvious in retrospect and completely invisible to the managing partner before the research: three of his six directly comparable Ahmedabad competitors had, over the preceding 18–24 months, deliberately reduced their revenue dependence on national FMCG brands from approximately 70–75% of portfolio revenue to 40–50% by adding premium regional, specialty, and D2C brand partnerships that offered 18–28% distributor margins against the 7–10% their national brand counterparts were paying.

The competitor that had moved furthest in this direction, a business of comparable revenue size to the managing partner’s, had increased its blended gross margin from approximately 12% to 21% over 18 months, with minimal revenue impact, simply by replacing 3 national brand lines with 5 premium regional equivalents in the same product categories.

This strategic shift was not visible from the outside. The competitors in question were still presenting as FMCG distributors. They were still serving the same retail base. They were still working with national brands, just with proportionally less reliance on them. The managing partner had sat next to these competitors at trade events for years and had no idea this transformation had occurred in their businesses.

Seven Premium Regional and D2C Brands Were Actively Seeking Ahmedabad Distribution, and No One Had Called Them

The supply-side brand mapping produced a finding with immediate commercial application: the research team identified seven premium FMCG brands, four in packaged food and snacking, two in health and wellness personal care, and one in household care, that were:

- Actively seeking Ahmedabad-based distribution representation

- Offering distributor margins of 20–27%

- Underrepresented or completely absent from organised Ahmedabad retail

- Targeting the same kiranas and modern trade accounts that the managing partner already served

Three of the seven brands had received venture capital funding in the preceding 12 months and had explicit Ahmedabad market entry targets as part of their investor-committed distribution expansion milestones. They needed a distributor. They needed one with established retail relationships. They would pay for quality.

The managing partner had never contacted any of them. Not because he had evaluated and declined, but because he had never heard of them. His sourcing process for new brand authorisations was entirely inbound and relationship-driven: he added brands when principals called him, not through systematic identification of brands that were actively seeking him.

The Retail Base Was Already Asking for These Brands

The structured conversations with retail category managers and organised trade buyers produced confirmation data that the research team had not expected to be as consistent as it was: across all 6 retail conversations, the recurring theme was unprompted interest in premium regional and D2C FMCG brands as an alternative to the national brand monoculture that dominated their shelves.

The specific language across multiple conversations was consistent: margins on national FMCG brands had made those lines increasingly marginal for independent retailers, who were actively looking for alternatives that offered both better retailer margins and the kind of distinctive product positioning that would bring in customers who could not simply compare prices with organised modern trade. The premium regional brands identified in Finding 2 fit this profile precisely.

Three of the retail category managers specifically mentioned brand names that appeared on the SAI GENiUS brand mapping list brands they had tried to source but had been unable to find an Ahmedabad distributor for. The demand was present, documented, and practically expressed. The supply infrastructure was absent. The managing partner was positioned to fill the gap if he moved before his competitors identified the same opportunity.

A Portfolio Reallocation Strategy, Activated Within 30 Days

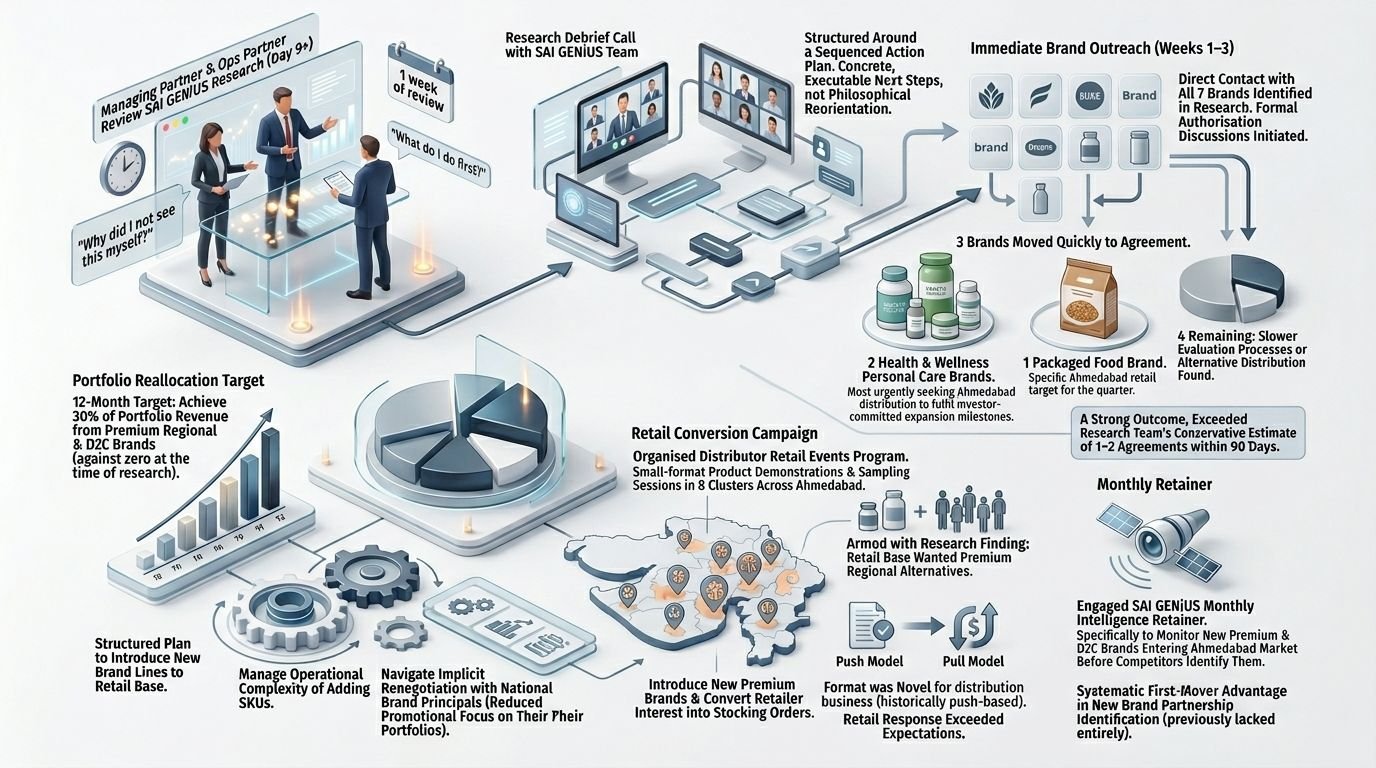

The managing partner received the SAI GENiUS research on Day 9 and spent the following week reviewing it with his operations partner. The response was, by his account, a combination of "why did I not see this myself" and "what do I do first."

The research debrief call with the SAI GENiUS team was structured around a sequenced action plan rather than a general strategic discussion because the findings pointed to concrete, executable next steps, not philosophical reorientation.

Immediate Brand Outreach (Week 1–3): The managing partner made direct contact with all seven brands identified in the research within three weeks. Formal authorisation discussions were initiated with all seven. Three brands moved quickly to an agreement the two health and wellness personal care brands (which were the most urgently seeking Ahmedabad distribution to fulfil investor-committed expansion milestones) and one packaged food brand that had a specific Ahmedabad retail target for the quarter.

The remaining four brands were either in slower evaluation processes or had since found alternative distribution approaches. Three active agreements in the first round were a strong outcome and exceeded the research team's conservative estimate of 1–2 agreements within 90 days.

Portfolio Reallocation Target: The managing partner set a 12-month target: achieve 30% of portfolio revenue from premium regional and D2C brands (against zero at the time of research). This required a structured plan to introduce the new brand lines to his retail base, manage the operational complexity of adding SKUs, and navigate the implicit renegotiation with national brand principals who would observe a reduction in his promotional focus on their portfolios.

Retail Conversion Campaign: Armed with the research finding that his own retail base was actively asking for premium regional alternatives, the managing partner organised a distributor retail events program, small-format product demonstrations and sampling sessions in 8 clusters of his retail base across Ahmedabad, to introduce the new premium brands and convert retailer interest into stocking orders. The format was novel for his distribution business, which had historically operated on a push-based order-and-deliver model. The retail response exceeded expectations.

Monthly Retainer: The managing partner engaged a SAI GENiUS monthly intelligence retainer specifically to monitor new premium and D2C brands entering the Ahmedabad market before his competitors identified them, giving him a systematic first-mover advantage in new brand partnership identification that he had previously lacked entirely.

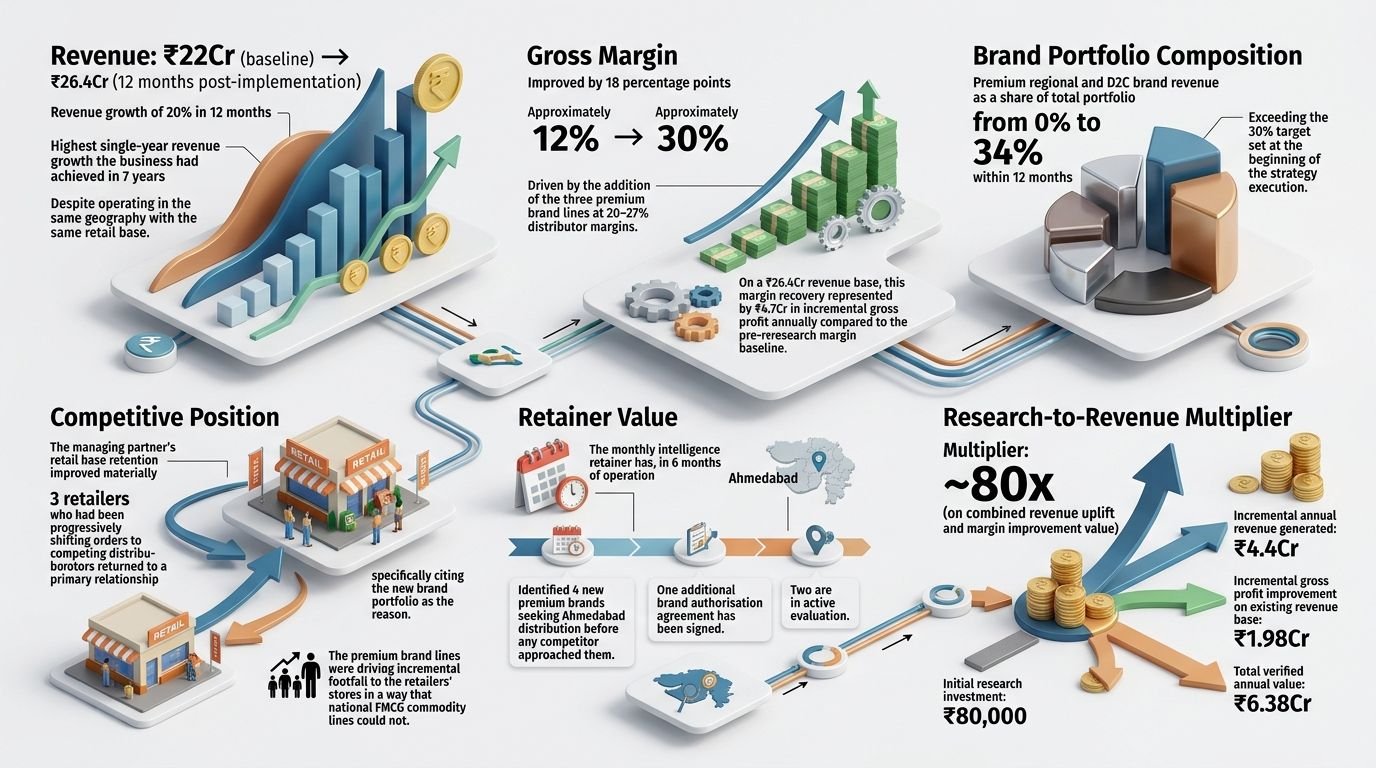

18-Point Margin Recovery and ₹4.4 Crore in Revenue Growth

Revenue: ₹22Cr (baseline) → ₹26.4Cr (12 months post-implementation). Revenue growth of 20% in 12 months, the highest single-year revenue growth the business had achieved in 7 years, despite operating in the same geography with the same retail base.

Gross Margin: Improved by 18 percentage points from approximately 12% to 30%, driven by the addition of the three premium brand lines at 20–27% distributor margins. On a ₹26.4Cr revenue base, this margin recovery represented approximately ₹4.7Cr in incremental gross profit annually compared to the pre-research margin baseline.

Brand Portfolio Composition: Premium regional and D2C brand revenue as a share of total portfolio: increased from 0% to 34% within 12 months, exceeding the 30% target set at the beginning of the strategy execution.

Competitive Position: The managing partner's retail base retention improved materially: 3 retailers who had been progressively shifting orders to competing distributors returned to a primary relationship, specifically citing the new brand portfolio as the reason. The premium brand lines were driving incremental footfall to the retailers' stores in a way that national FMCG commodity lines could not.

Retainer Value: The monthly intelligence retainer has, in 6 months of operation, identified 4 new premium brands seeking Ahmedabad distribution before any competitor approached them. One additional brand authorisation agreement has been signed. Two are in active evaluation.

Research-to-Revenue Multiplier: Initial research investment: ₹80,000. Incremental annual revenue generated: ₹4.4Cr. Incremental gross profit improvement on existing revenue base: ₹1.98Cr. Total verified annual value: ₹6.38Cr. Multiplier: ~80x (on combined revenue uplift and margin improvement value).