CASE STUDY — Corporate Strategy Team | M&A Intelligence Retainer | IT Services | Mumbai

CASE STUDY

IT Services (Mid-Market Indian IT Company)

Mumbai, Maharashtra

Corporate (₹180Cr annual revenue; listed entity subsidiary)

Ongoing Competitive Intelligence Retainer + M&A Target Identification + Acquisition Readiness Monitoring

₹55,000/month (retainer) — 6 months prior to acquisition identification

Ongoing (acquisition target identified in Month 4 of retainer)

Initiated direct acquisition approach to a Pune cybersecurity consulting firm identified through retainer intelligence — before any competitor was in conversation

Acquisition completed at "a full turn below" competitive process valuation; ₹40Cr addressable market expansion; 3 new enterprise clients added; GCC cybersecurity capability built

Not fully quantified (M&A transaction value confidential; ₹40Cr addressable market expansion documented)

CLIENT VOICE

"The intelligence brief that flagged the Pune firm was exactly what we had designed the retainer to produce — a pre-process identification of an acquisition-ready target before anyone else was in conversation. What we did not fully anticipate was how specific and actionable the escalation report would be. The three signals the research team identified were not things we would have found through our standard monitoring. The warm introduction they identified for the first approach — that was the difference between walking in as a credible strategic partner and walking in as a cold acquirer. We closed a transaction at a valuation we could not have achieved in a competitive process. The retainer paid for itself before we finished reviewing the Month 4 brief."

— Head of Corporate Development, Mid-Market IT Services Company, Mumbai (Identity anonymized with permission)

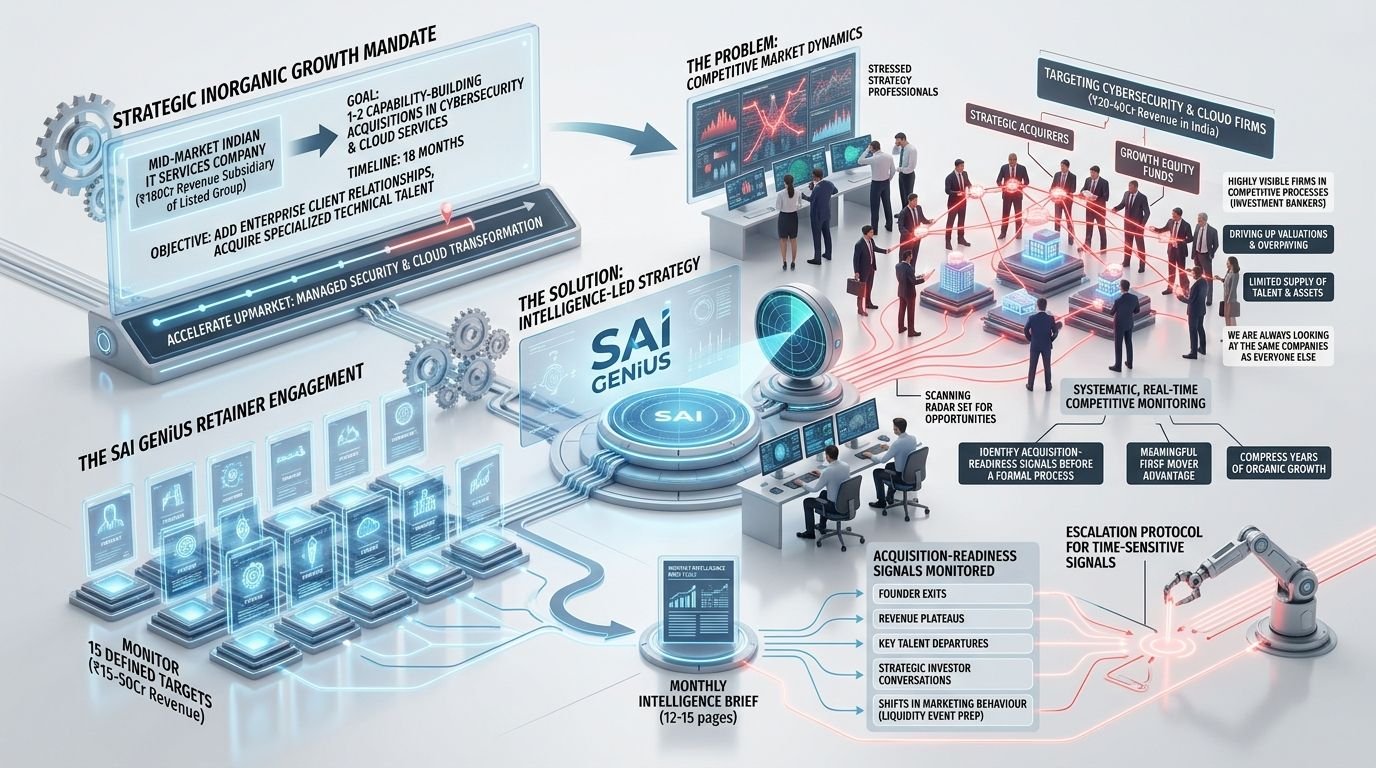

A Mid-Market IT Services Company, an Inorganic Growth Mandate, and the Classic Problem of Looking for Acquisitions in the Same Places as Everyone Else

The strategy team of a mid-market Indian IT services company a ₹180 crore revenue subsidiary of a listed corporate group had been given a specific inorganic growth mandate by its parent board: identify and execute one or two capability-building acquisitions in the cybersecurity and cloud services segments within 18 months, with a specific brief to add enterprise client relationships and specialized technical talent that would accelerate the company's move upmarket from mid-tier IT services into managed security and cloud transformation advisory.

The mandate was clear. The market was large. The acquisition logic was sound cybersecurity consulting demand in India was growing rapidly, the talent supply was constrained, and a well-priced acquisition of a specialist firm could compress years of organic capability building into a single transaction.

The problem was competitive dynamics. The strategy team's head of corporate development described the challenge precisely in the SAI GENiUS discovery call: "Every well-run cybersecurity and cloud consulting firm in India with ₹20–40Cr revenue has already been approached by at least one strategic acquirer or growth equity fund. The businesses we can see clearly, the ones with strong media presence, frequent speaking engagements, notable client names in press releases, are either in a process, have already closed, or are being managed by an investment banker who will run a competitive process and drive up the valuation. We are always looking at the same companies as everyone else, and we are always overpaying or losing."

The head of corporate development had worked with intelligence-led M&A processes in a previous role at a larger IT company and believed that systematic, real-time competitive monitoring specifically designed to identify acquisition-readiness signals before a formal process began could provide a meaningful first-mover advantage. But the company's internal research capacity was not structured for continuous competitive monitoring. They needed an external intelligence partner.

The SAI GENiUS retainer engagement began with a specific brief: monitor 15 defined cybersecurity and cloud services companies in the ₹15–50Cr revenue range, specifically for signals indicating acquisition readiness, founder exits, revenue plateaus, key talent departures, strategic investor conversations, or shifts in marketing behaviour indicating a company preparing for a liquidity event.

The 15 targets were defined collaboratively between the SAI GENiUS research team and the client's corporate development lead. The retainer was structured as a monthly intelligence brief, a 12–15 page document covering all 15 companies across the defined monitoring dimensions with an escalation protocol for time-sensitive signals requiring immediate attention.

Four Months of Monitoring, One Target, and a Signal No One Else Had Seen

For the first three months of the retainer, the monthly intelligence briefs delivered incremental intelligence across the 15 targets — useful background, competitive positioning updates, and several observations of companies whose growth trajectories were slowing — but no clear acquisition-readiness signal that met the threshold for the client's specific criteria.

Month 4 was different.

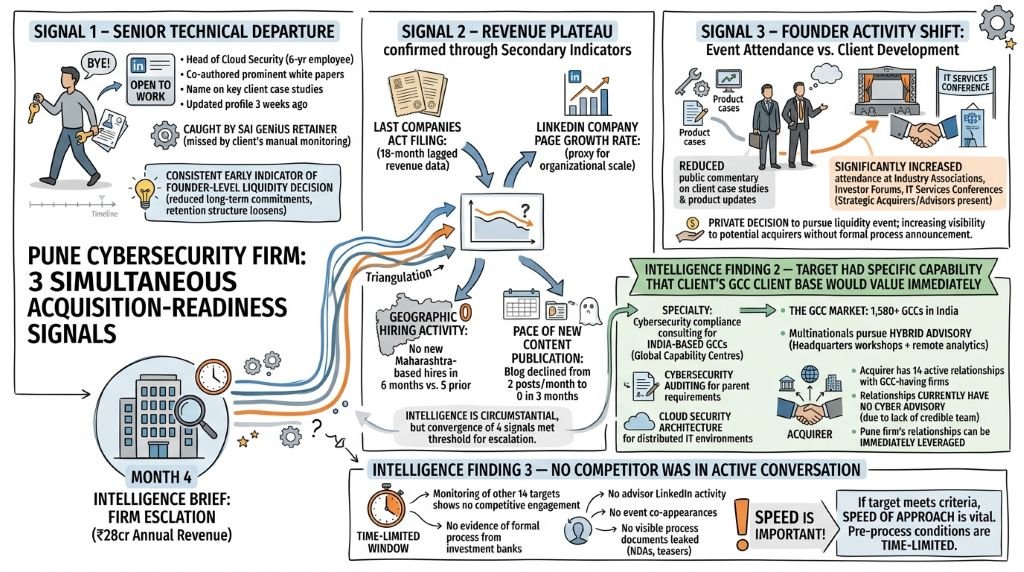

A Pune Cybersecurity Firm Was Showing Three Simultaneous Acquisition-Readiness Signals

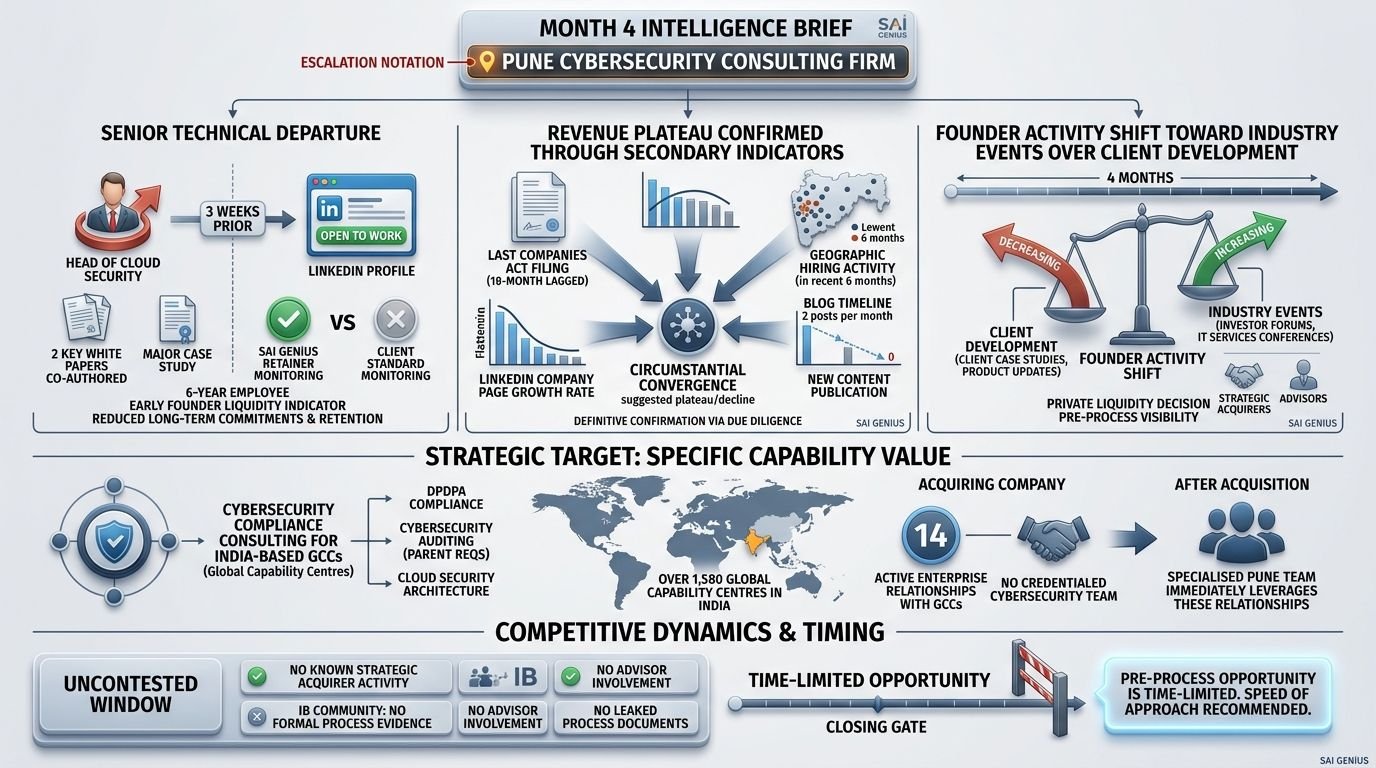

The Month 4 intelligence brief flagged one of the 15 monitored companies, a Pune-based cybersecurity consulting firm with approximately ₹28 crore in annual revenue, with an escalation notation indicating three simultaneous signals that, in the research team’s assessment, warranted immediate client attention.

Senior Technical Departure: LinkedIn activity monitoring identified that the company’s Head of Cloud Security, a 6-year employee who had co-authored the firm’s two most prominent technical white papers and whose name appeared on the firm’s most significant enterprise client case study references, had updated his LinkedIn profile to “Open to Work” 3 weeks prior. The profile update had not been visible in the client’s standard market monitoring because the client’s internal team did not conduct systematic LinkedIn monitoring of the 15 target companies. The SAI GENiUS retainer did.

Senior technical talent departure at this level is one of the most consistent early indicators of founder-level liquidity decision-making: when a founding team has made a private decision to pursue a sale, the first operational change is often a reduction in long-term hiring commitments and a loosening of retention structures for senior non-founder employees.

Revenue Plateau Confirmed Through Secondary Indicators: A triangulation of secondary data sources including the company’s last published Companies Act filing (which provided 18-month-lagged revenue data), its LinkedIn company page growth rate (a proxy indicator for organizational expansion or contraction), its geographic hiring activity (no new Maharashtra-based hires in 6 months, against 5 new hires in the preceding 6-month period), and the pace of new content publication on its company blog (which had declined from 2 posts per month to 0 in the preceding 3 months) suggested that the company’s revenue had plateaued or declined relative to the preceding year.

The intelligence was circumstantial; definitive revenue confirmation would require the acquisition due diligence process to validate. But the convergence of four independent secondary indicators pointing in the same direction met the research team’s threshold for escalation.

Founder Activity Shift Toward Industry Events Over Client Development: A systematic review of the two founders’ public LinkedIn activity over the preceding 4 months revealed a pattern that the research team had observed as a consistent acquisition-readiness indicator in prior competitive monitoring work: the founders had significantly increased their attendance at industry association events, investor forums, and IT services industry conferences forums where strategic acquirers and their advisors are typically present while simultaneously reducing their public commentary on client case studies and product development updates.

This pattern is consistent with a founder team that has made a private decision to pursue a liquidity event and is beginning the process of increasing their visibility to potential acquirers without formally announcing a process.

The Target Had a Specific Capability That the Client’s GCC Client Base Would Value Immediately

The Month 4 brief included a capability assessment section on the escalated target, specifically evaluating the relevance of its service portfolio to the client’s existing customer base and growth strategy.

The finding was directly relevant: the Pune firm had built a specific speciality in cybersecurity compliance consulting for India-based Global Capability Centres (GCCs) of multinational corporations, specifically, helping GCCs navigate India’s evolving data protection regulations (DPDPA compliance), cybersecurity auditing for parent-company regulatory requirements, and cloud security architecture for distributed multinational IT environments.

More than 1,580 global capability centres already operate in India, with multinational corporations increasingly pursuing hybrid advisory engagements that combine headquarters workshops with remote analytics delivery. The GCC cybersecurity compliance segment was therefore not an academic growth opportunity; it was a present, active, high-value client category where the acquiring company currently had no specialised capability and where the Pune firm’s existing client relationships could be immediately leveraged through the acquirer’s broader enterprise client network.

The acquiring company had 14 active enterprise relationships with companies that had India-based GCCs. None of those relationships currently included cybersecurity advisory services because the company had no credible cybersecurity team to sell through. The acquisition would change that immediately.

No Competitor Was in Active Conversation

The research team’s monitoring of the other 14 targets in the retainer brief included a cross-referential tracking of known strategic acquirer activity. None of the 5 strategic IT services acquirers that the client’s corporate development team had identified as most likely competitors for cybersecurity acquisition targets had any publicly or semi-publicly visible engagement with the Pune firm.

The investment banking community’s coverage of the firm showed no evidence of a formal process: no advisor LinkedIn activity in the firm’s orbit, no event co-appearances between the founders and known M&A advisors in the IT services space, no visible process documents (NDAs, teaser emails) that had leaked into industry network conversations.

The window was real. It was also potentially short the acquisition-readiness signals the research team had identified were, by their nature, signals that multiple observers could theoretically identify independently. The recommendation in the Month 4 brief was unambiguous: “If this target meets the client’s acquisition criteria upon initial outreach, speed of approach is important. The conditions that create a pre-process opportunity are time-limited.”

A Direct Approach, Structured for Relationship Rather Than Transaction

The client's head of corporate development reviewed the Month 4 brief within 48 hours of receipt and brought it to the Managing Director with a recommendation: initiate a direct, non-transactional approach to the Pune firm's founders within 2 weeks.

The approach strategy was deliberate and unconventional in its framing. Rather than approaching the founders through an intermediary or with an explicit acquisition inquiry — which would immediately put them on the defensive and potentially trigger a formal process with other suitors — the corporate development team used a warm introduction identified in the SAI GENiUS research: a mutual contact at a Maharashtra IT industry association who knew both the Pune firm's founders and the client's managing director personally.

The introductory conversation was framed as a potential strategic partnership discussion — exploring whether a subcontracting or joint go-to-market relationship in the GCC cybersecurity space would be mutually beneficial. This framing was genuine: a partnership would have been a viable alternative to an acquisition if the founders had not been in acquisition-ready mode.

The first meeting confirmed the intelligence. Within 60 minutes of the initial conversation, the Pune firm's lead founder made an unprompted reference to "thinking about the long-term future of the firm" and expressed interest in understanding what "a closer working relationship" might look like. The signal was unambiguous to the experienced corporate development lead.

Formal acquisition discussions began in the third meeting. No investment banker was engaged by the target firm throughout the process — the direct approach had established a relationship that the founders preferred to manage personally rather than through an intermediary.

An Acquisition Completed at Below-Market Valuation, ₹40Cr of Addressable Market Unlocked, and a GCC Capability Built

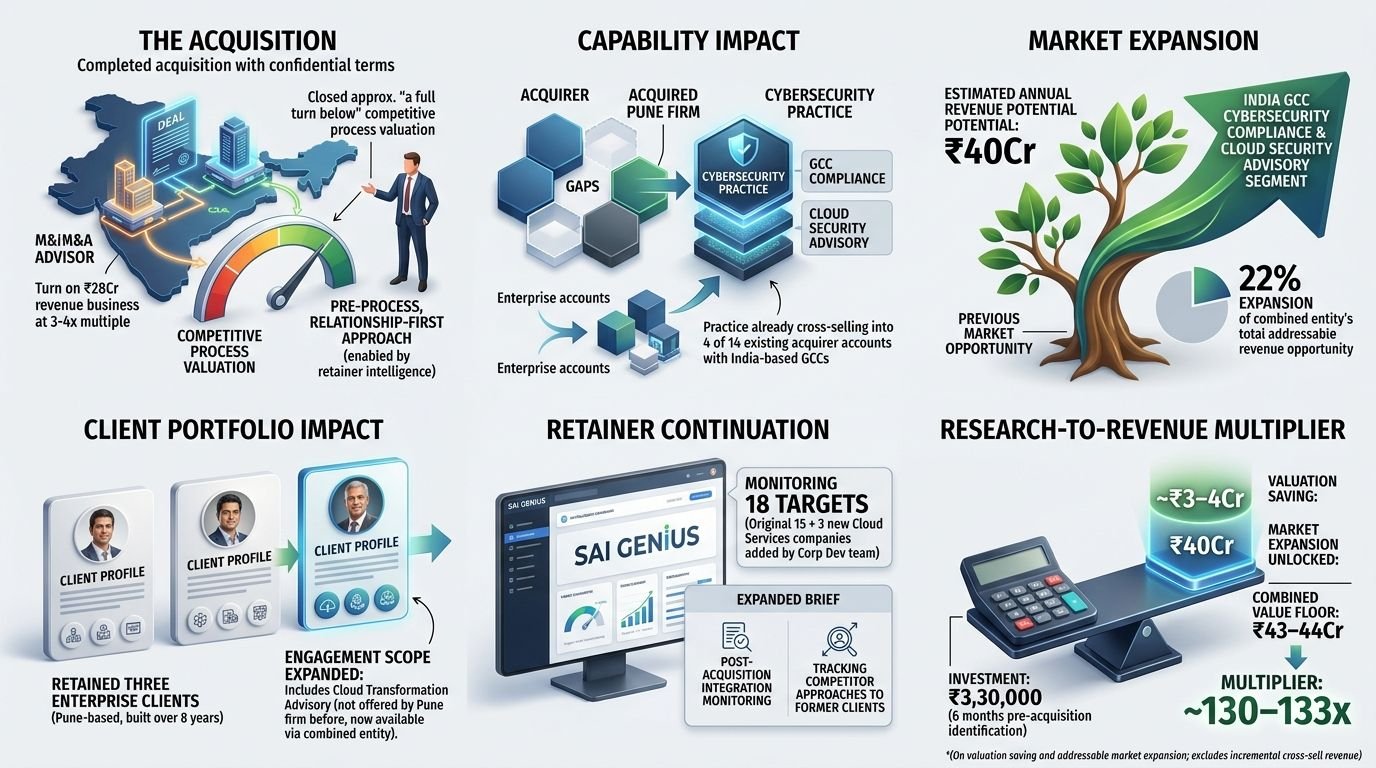

The Acquisition: The acquisition was completed. Terms are confidential at the client's request. The client's M&A advisor, engaged for due diligence and transaction structuring after the negotiation framework was established, noted that the acquisition had closed at approximately "a full turn below" the valuation that a formal competitive process would likely have generated for a firm with the target's revenue profile and client relationships. In the Indian IT services M&A market, a "turn" on a ₹28Cr revenue business at a 3–4x revenue multiple implies a valuation difference of approximately ₹3–4Cr in the client's favour, a function entirely of the pre-process, relationship-first approach enabled by the retainer intelligence.

Capability Impact: The combined entity has a cybersecurity practice capable of addressing the GCC compliance and cloud security advisory market, a capability the acquiring company had no access to before the acquisition. The practice is already cross-selling into 4 of the acquirer's 14 existing enterprise accounts that have India-based GCCs.

Market Expansion: The addressable market expansion from the acquisition, specifically the India GCC cybersecurity compliance and cloud security advisory segment, is estimated at ₹40Cr in annual revenue potential across the combined entity's addressable enterprise client base. This represents a 22% expansion of the combined entity's total addressable revenue opportunity.

Client Portfolio Impact: Three of the Pune firm's existing enterprise client relationships, which the founding team had built over 8 years in the Pune market, were retained through the acquisition transition and added to the combined entity's client portfolio. One of the three has already expanded its engagement scope to include cloud transformation advisory, a capability the Pune firm had not offered, but the combined entity does.

Retainer Continuation: The SAI GENiUS competitive intelligence retainer is ongoing, now monitoring 18 targets (the original 15 plus 3 newly identified cloud services companies the client's corporate development team has added following the acquisition). The retainer brief has been expanded to include post-acquisition integration monitoring, specifically tracking whether any of the acquired firm's competitors move to approach its former clients during the integration period.

Research-to-Revenue Multiplier: Retainer investment (6 months pre-acquisition identification): ₹3,30,000. Valuation saving versus competitive process: approximately ₹3–4Cr (conservative estimate based on M&A advisor's "full turn below" characterisation). Addressable market expansion unlocked: ₹40Cr. Combined value floor: ₹43–44Cr. Multiplier: ~130–133x (on valuation saving and addressable market expansion; does not include incremental revenue already generated from cross-sell to acquired firm's clients).