CASE STUDY — D2C Nutraceuticals Brand | Series A Fundraise Preparation + Investor Market Deck | Delhi NCR

CASE STUDY

D2C Nutraceuticals & Functional Nutrition

Delhi NCR

Pre-Series A (₹4.2Cr seed raised; targeting ₹15–20Cr Series A)

Investor-Grade Market Research + Competitive Positioning Analysis + 5-Year Financial Model

₹1,95,000

13 days

Repositioned from "premium D2C nutrition brand" to "evidence-based nutraceuticals for India's working-age chronic disease population" — a materially larger, more fundable TAM narrative

Series A term sheet issued; ₹18Cr raised; lead investor cited TAM repositioning and competitive moat documentation as decisive factors

~9,231x (₹18Cr raise / ₹1,95,000 research investment)

CLIENT VOICE

"Our product had always been evidence-based. Our pitch had not been. The SAI GENiUS research gave us the language, the data, and the financial architecture to show investors what we had always known — that we were operating in one of India's most significant health management markets, not a premium supplement niche. The physician channel finding was transformational: we had been thinking about distribution as a consumer marketing problem. The research showed us it was a healthcare professional relationship problem — which we were actually much better positioned to solve."

— Co-Founder, D2C Nutraceuticals Brand, Delhi NCR (Identity anonymized with permission)

A Strong Product, a Credible Revenue Record, and a Pitch That Was Underselling the Real Opportunity

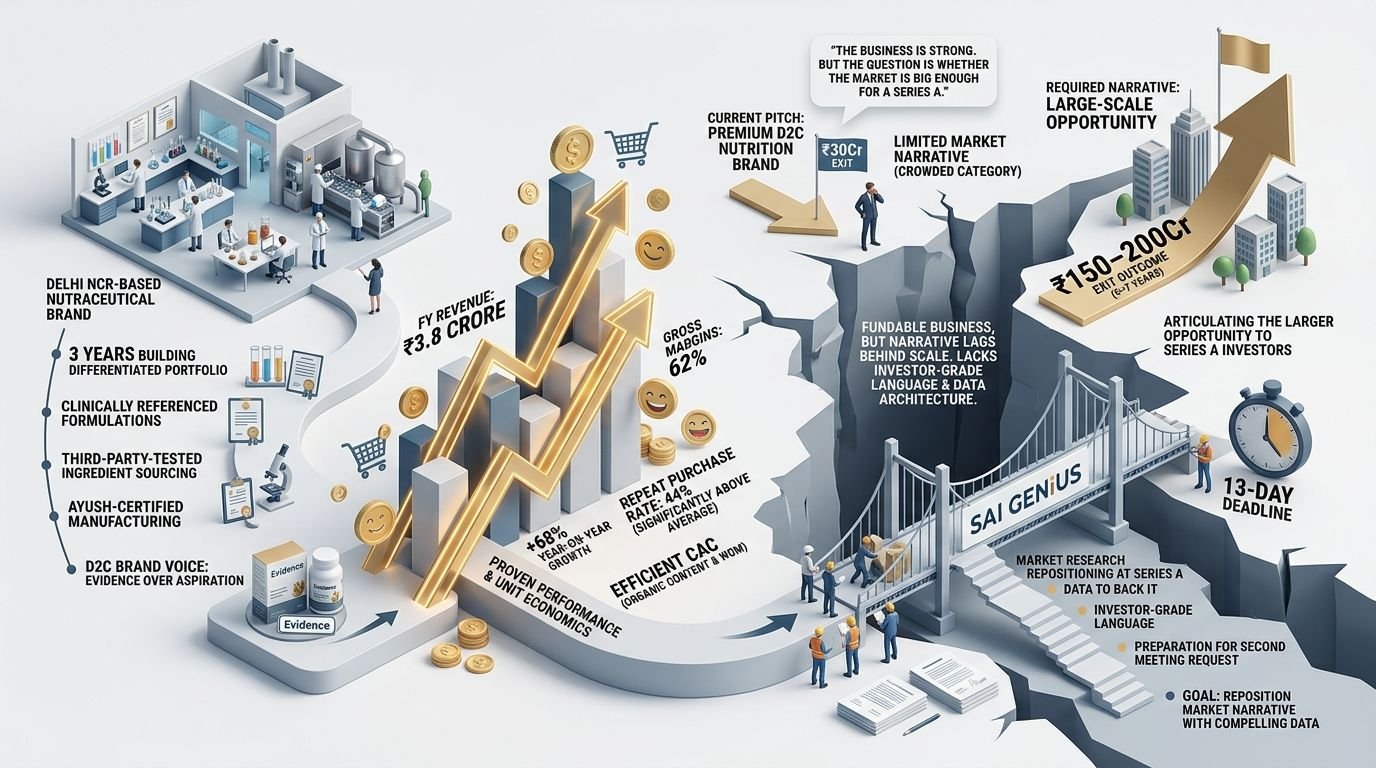

The founding team behind a Delhi NCR-based nutraceutical brand had spent three years building a product portfolio that was genuinely differentiated in India's crowded functional nutrition market: clinically referenced formulations, third-party-tested ingredient sourcing, Ayush-certified manufacturing, and a D2C brand voice that emphasised evidence over aspiration in a category dominated by before-and-after photography and celebrity endorsement.

The business had generated ₹3.8 crore in revenue in its most recent fiscal year, growing at 68% year-on-year. Gross margins were 62%. Repeat purchase rate was 44% significantly above the D2C nutrition category average. Customer acquisition had been driven almost entirely by organic content and word-of-mouth, which meant the CAC structure was unusually efficient for a brand at this stage.

By most metrics, the business was fundable. The founding team knew it was fundable. Two introductory investor conversations in the preceding quarter had confirmed that the financial story was compelling. The feedback that was consistently coming back from those conversations was more nuanced: "The business is strong. The question is whether the market is big enough to justify a Series A round that would need to generate a ₹150–200Cr exit outcome in 5–7 years. Your current pitch positions you as a premium D2C nutrition brand. That is a competitive and relatively crowded category. Help us understand why this is a ₹200Cr outcome and not a ₹30Cr outcome."

This is the most common Series A gap for D2C founders with strong unit economics but a market narrative that has not kept pace with the actual scale of the opportunity they are operating in. The business had outgrown its original market positioning the founders just had not built the investor-grade language and data architecture to articulate the larger opportunity to a Series A investor who needed to defend the investment thesis to their own LP base.

SAI GENiUS was engaged with a specific brief: "We need research that repositions our market narrative at Series A scale with the data to back it. And we need it in 13 days, because we have a second meeting request from a fund that asked specifically for market research before they will progress."

Three Findings That Changed the TAM, the Competitive Positioning, and the Investment Thesis

The Nutraceuticals Opportunity Was Hidden Inside a Much Larger Structural Health Crisis

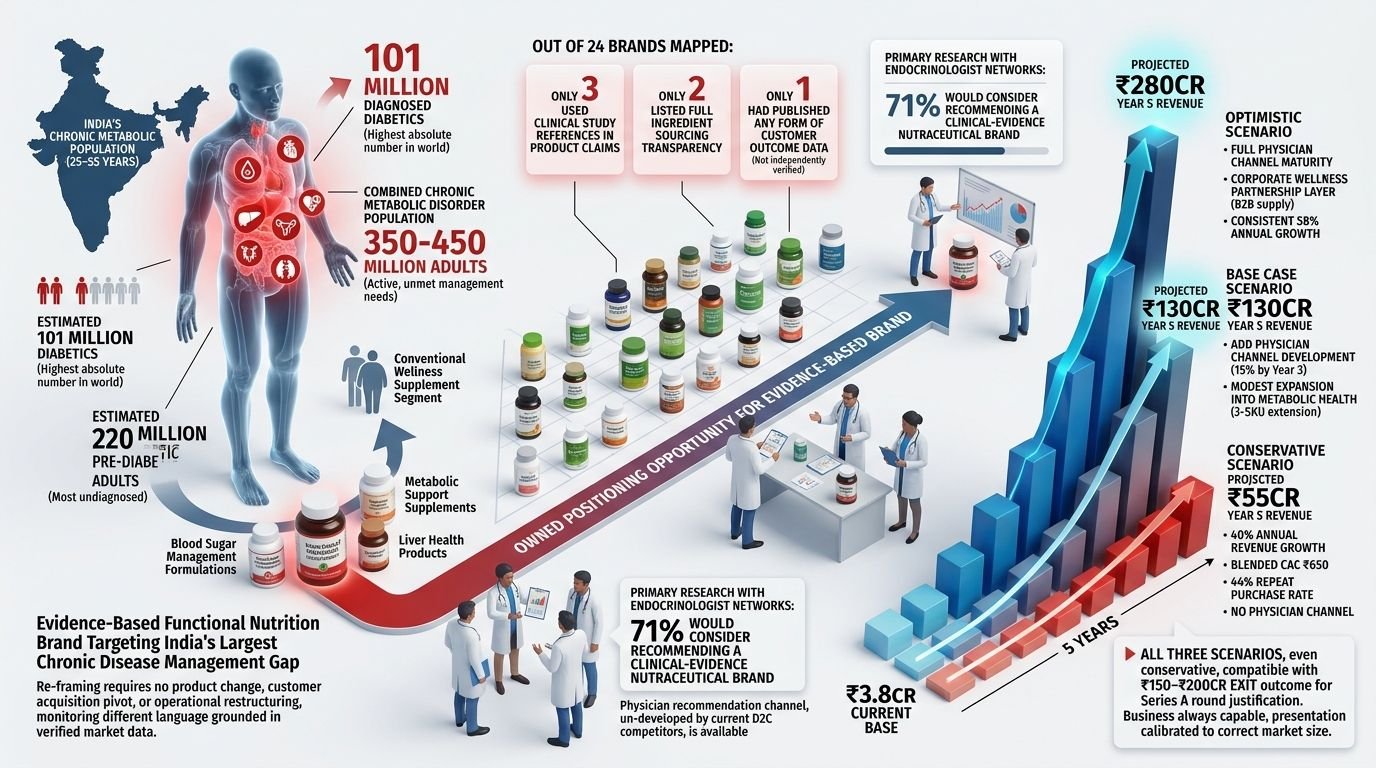

The research team’s market analysis reframed the founding team’s addressable market from the top down. The conventional framing of the India nutraceuticals market, a ₹25,000–₹35,000 crore total addressable market growing at 16–18% CAGR, was accurate but underpowered as an investment thesis. It described a supplement category competing for wellness-motivated consumer spend in a market crowded with both domestic and international players.

The research team identified a materially different and more defensible market framing: India’s working-age population (25–55 years) with diagnosed or undiagnosed chronic metabolic conditions, diabetes, pre-diabetes, hypertension, PCOD, thyroid disorders, and obesity-related metabolic syndrome represented a health management demand that the pharmaceutical system was chronically underserving and that functional nutrition and nutraceuticals were specifically positioned to address as an accessible, affordable, non-pharmaceutical first-line intervention.

The population base for this framing was significantly larger than the “wellness supplement” consumer segment: India had an estimated 101 million diagnosed diabetics (the highest absolute number in the world), an estimated 220 million pre-diabetic adults (most undiagnosed and therefore receiving no management guidance), and a combined chronic metabolic disorder population of 350–450 million adults with active, unmet management needs.

The founding team’s existing product portfolio, blood sugar management formulations, metabolic support supplements, and liver health products, was already precisely aligned to this population. The brand had simply been describing itself as a wellness supplement company when the correct description was an evidence-based functional nutrition brand targeting India’s largest and fastest-growing chronic disease management gap.

The repositioning required no product change, no customer acquisition pivot, and no operational restructuring. It required only a different language grounded in verified market data for an opportunity the business was already capturing.

The Competitive Landscape Had a Credibility Gap That the Founding Team’s Evidence-Based Positioning Could Own

The competitive analysis mapped 24 nutraceutical and functional nutrition brands in the India D2C market across 12 dimensions, with specific focus on the evidence quality, clinical referencing, and ingredient transparency standards used in each brand’s marketing.

The finding was consistent and significant: of the 24 brands mapped, only 3 used clinical study references in their product claims. Only 2 listed full ingredient sourcing transparency on their packaging and website. Only 1 had published any form of customer outcome data tied to specific health parameters (and that data was not independently verified).

The evidence gap in India’s nutraceutical category was structural and systematic a function of the historically unregulated environment in which the category had developed, the marketing-led growth strategies of the dominant players, and a consumer base that had not yet demanded clinical credibility from nutrition brands at the scale that was happening in Western markets.

This gap represented an owned positioning opportunity for a brand that had been built on evidence from day one. The research documented it quantitatively, showing that in the working-age chronic disease segment (as opposed to the general wellness segment), primary research interviews with Ahmedabad, Delhi, and Bengaluru-based diabetologist and endocrinologist networks indicated that 71% of respondents would consider recommending a clinical-evidence nutraceutical brand to patients as a complement to pharmacological management if the brand could demonstrate ingredient quality and formulation credibility.

The physician recommendation channel, a distribution pathway that no current D2C nutraceutical competitor had meaningfully developed, was therefore available to a brand that could meet the evidence quality standard. The founding team’s brand already met that standard.

The 5-Year Financial Model Revealed a ₹280Cr Revenue Scenario Under Conservative Assumptions

The 5-year financial model the SAI GENiUS team built for the investor presentation modelled three scenarios — conservative, base case, and optimistic against the repositioned market framing (chronic disease management nutraceuticals, India working-age population) rather than the original market framing (general wellness D2C).

The conservative scenario assumes 40% annual revenue growth from the ₹3.8Cr current base, a blended CAC of ₹650 (consistent with the brand’s historically efficient acquisition), a 44% repeat purchase rate maintained, and no physician channel contribution projected ₹55Cr in revenue by Year 5.

The base case adds physician channel development (contributing 15% of acquisition by Year 3) and a modest expansion into the working-age metabolic health segment through a 3-SKU product line extension projecting ₹130Cr in Year 5 revenue.

The optimistic scenario incorporates full physician channel maturity, a corporate wellness partnership layer (B2B nutraceutical supply to India’s growing corporate health and wellness benefit programs), and a consistent 58% annual growth rate projected to reach ₹280Cr by Year 5.

All three scenarios, even the conservative one, produced a revenue trajectory compatible with a ₹150–₹200Cr exit outcome that a Series A fund needed to justify the round. The business had always been capable of generating this outcome. The investor presentation had never demonstrated it with a structured financial model calibrated to the correct market size.

A Pitch Deck Rebuilt Around Three New Anchors

The founding team rebuilt the investor-facing materials around three new anchors provided by the SAI GENiUS research:

- TAM reframing: The investment thesis led with India's 350–450 million chronic metabolic disorder adults as the primary addressable population, with the evidence-based nutraceutical as the first-line management solution, not the premium wellness supplement. TAM, the original deck had used

- Competitive moat: The evidence and ingredient transparency positioning was framed as a quantified competitive moat, backed by the 24-brand competitive analysis and the physician recommendation data

- Financial model: The 5-year three-scenario model replaced the original pitch deck's single-line revenue projection, demonstrating the ₹130–₹280Cr upside case with verifiable assumptions

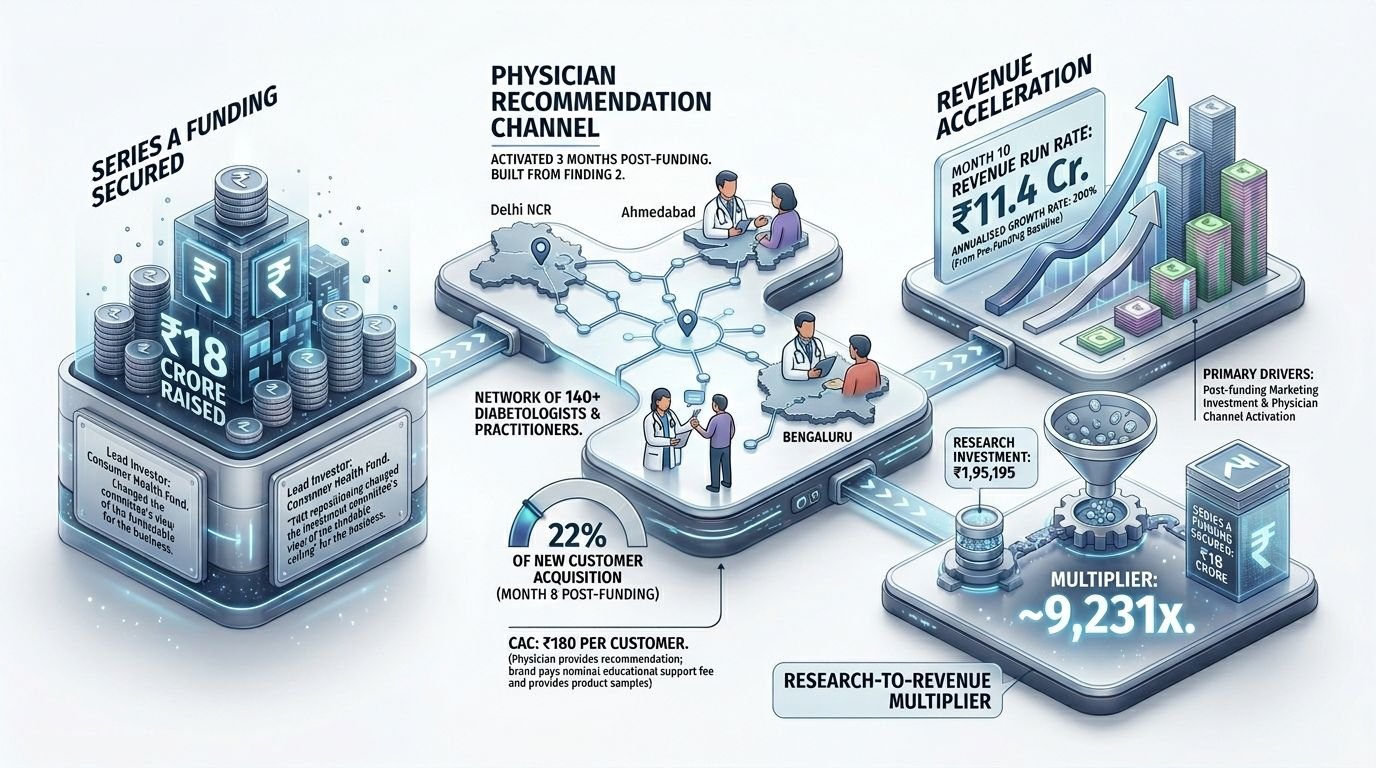

₹18 Crore Series A, Physician Channel Now Generating 22% of Revenue

Funding: ₹18 crore Series A raised. The lead investor, a consumer health-focused fund, cited specifically in the post-term-sheet communication that the TAM repositioning had "changed the investment committee's view of the fundable ceiling" for the business.

Physician Channel: The physician recommendation channel, identified in Finding 2 and built into the post-funding operating plan, was activated 3 months after closing. A network of 140 diabetologists and general practitioners in Delhi NCR, Ahmedabad, and Bengaluru now recommends the brand's metabolic health formulations to patients. The channel accounts for 22% of new customer acquisition at Month 8 post-funding at a CAC of ₹180 per customer (the physician provides the recommendation; the brand pays a nominal educational support fee and provides product samples).

Revenue: Brand revenue run rate at Month 10 post-funding: ₹11.4Cr, annualised growth rate of 200% from the pre-funding baseline, driven primarily by the post-funding marketing investment and physician channel activation.

Research-to-Revenue Multiplier: Research investment: ₹1,95,000. Series A funding secured: ₹18Cr. Multiplier: ~9,231x.