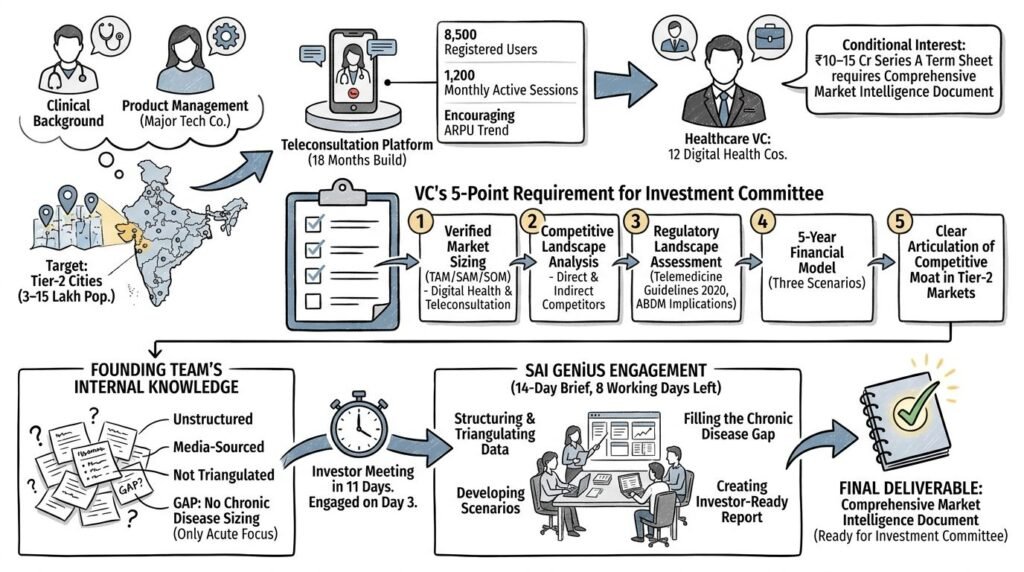

Two co-founders — one with a clinical background, one with a product management background from a major Indian technology company — had spent 18 months building a teleconsultation platform specifically targeting Tier-2 Indian cities. Their insight was precise: India's primary care gap was not in metros (where telemedicine had meaningful penetration), but in cities of 3–15 lakh population where specialist access was limited, travel costs were prohibitive, and digital health adoption was accelerating through smartphone and internet expansion.

Their seed-funded product had 8,500 registered users, 1,200 monthly active teleconsultation sessions, and an ARPU trend line that was encouraging but not yet sustained.

A lead investor — a healthcare-focused VC with a portfolio of 12 Indian digital health companies — had reviewed the initial pitch deck and expressed conditional interest. The condition: before issuing a term sheet for a ₹10–15 crore Series A, they needed a comprehensive market intelligence document that would support their own internal investment committee presentation.

Specifically, the investor requested:

- Multi-source verified market sizing (TAM/SAM/SOM) for India's digital health and teleconsultation market

- Competitive landscape analysis covering direct and indirect competitors

- Regulatory landscape assessment (Telemedicine Practice Guidelines 2020; ABDM implications)

- 5-year financial model with three scenarios

- A clear articulation of the competitive moat in Tier-2 markets

The investor meeting was in 11 days.

The founding team had internal market research, assembled over 18 months of operating in the space. But it was accumulated knowledge, not a structured document. It was partially sourced from media coverage and competitor press releases. It had not been triangulated. And it had a specific gap: the founders had never formally sized the chronic disease management opportunity in Tier-2 India, because they had positioned their platform as an acute primary care solution.

SAI GENiUS was engaged with a 14-day brief on Day 3 after the investor call.

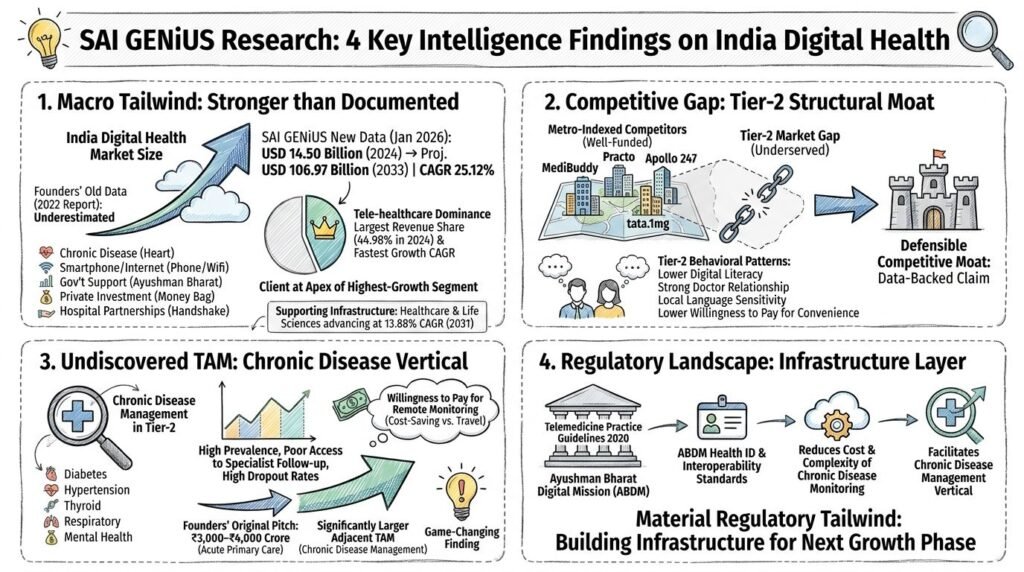

The SAI GENiUS research team delivered a 58-page investor-grade market intelligence document covering all five investor-requested components. The research was conducted across primary and secondary sources over 12 days, with the document formatted and delivered on Day 14 — 3 days before the investor meeting.

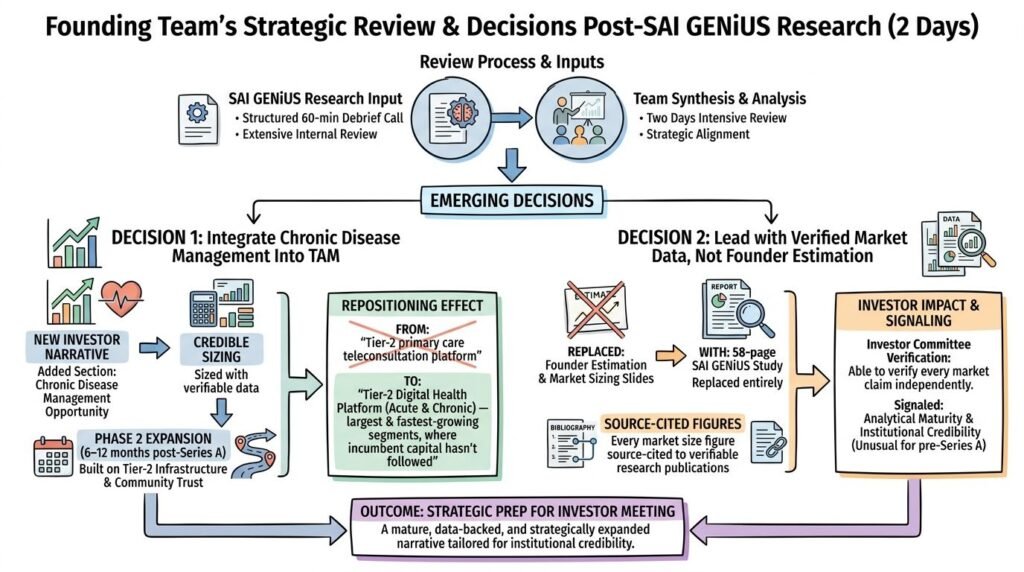

The founding team spent two days with the SAI GENiUS research — the structured 60-minute debrief call and extensive internal review — before their investor meeting. Two specific decisions emerged from that review.

Decision 1 — Integrate Chronic Disease Management Into the TAM

The founding team added a new section to their investor narrative: a clearly articulated chronic disease management opportunity, sized credibly with verifiable data, positioned as Phase 2 product expansion (6–12 months post-Series A) built on the same Tier-2 infrastructure and community trust the core platform was already developing.

This repositioned the company from "a Tier-2 primary care teleconsultation platform" to "a Tier-2 digital health platform capturing both acute and chronic care — the two largest and fastest-growing segments of India's teleconsultation market, in the one geography where incumbent capital has not followed."

Decision 2 — Lead with Verified Market Data, Not Founder Estimation

The 58-page SAI GENiUS study replaced the market sizing slides in the pitch deck entirely. Every market size figure was source-cited to verifiable research publications. The investor committee reviewing the internal investment memo would be able to verify every market claim independently. This level of evidentiary rigor — unusual for a pre-Series A pitch — signaled analytical maturity and institutional credibility that the founding team's internal research could not have produced.

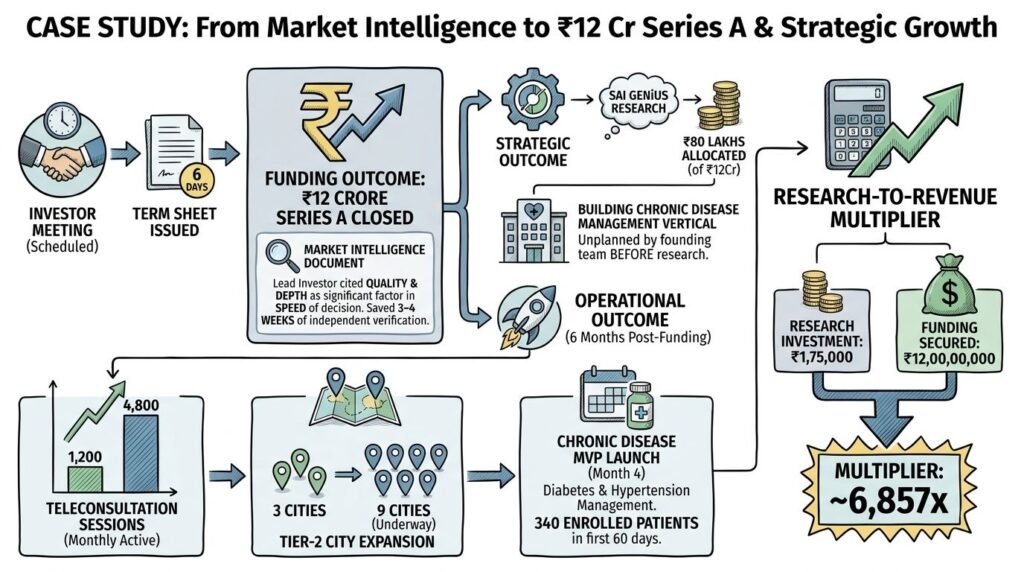

The investor meeting proceeded as scheduled. The term sheet was issued 6 days later.

Funding Outcome: ₹12 crore Series A closed. The lead investor cited the quality and depth of the market intelligence document as a significant factor in the speed of the investment committee's decision — a decision that might have taken 3–4 additional weeks of back-and-forth had the market intelligence required independent verification.

Strategic Outcome: ₹80 lakhs of the ₹12Cr raise was specifically allocated — within the first post-funding operating plan — to building the chronic disease management vertical identified in the SAI GENiUS research. A vertical the founding team had not been planning to build before the research.

Operational Outcome: Six months post-funding, the platform's monthly active teleconsultation sessions grew from 1,200 to 4,800. Tier-2 city expansion from 3 cities to 9 cities is underway. The chronic disease management MVP (diabetes and hypertension management) launched in month 4 post-funding, with 340 enrolled chronic disease patients in the first 60 days.

Research-to-Revenue Multiplier: Research investment: ₹1,75,000. Funding secured: ₹12,00,00,000. Multiplier: ~6,857x.