The Most Cited Gap in Indian Finance and the Most Misunderstood

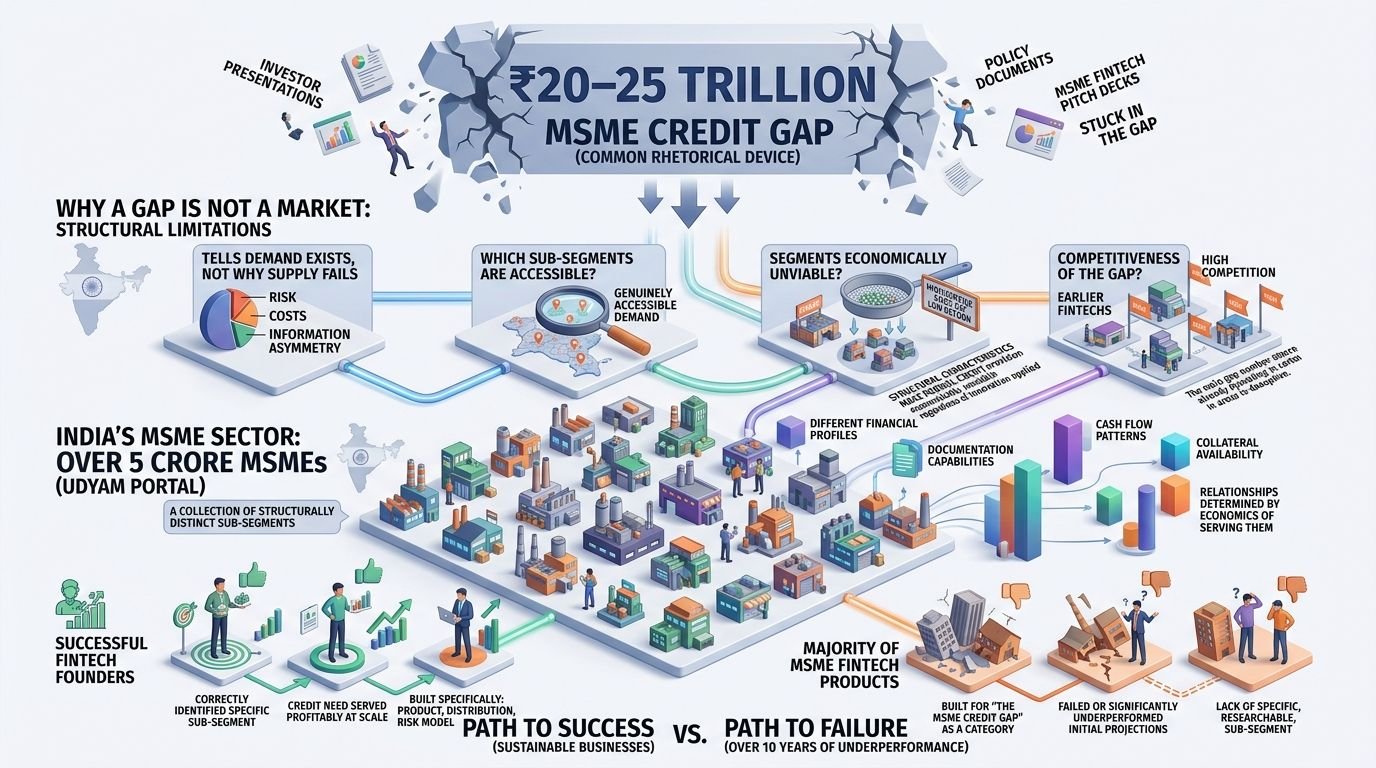

The ₹20–25 trillion MSME credit gap has been cited so frequently, in so many investor presentations and policy documents, that it has become one of those market facts that functions more as a rhetorical device than as a strategic input. Every MSME FinTech pitch deck in India contains some version of it. Most of them contain very little else about the market beyond it.

The problem with using the credit gap as a market opportunity statement is structural: a gap is not a market. A gap tells you that demand exists and supply does not meet it. It does not tell you why the supply does not meet it, which specific sub-segments of demand are genuinely accessible, which segments have structural characteristics that make formal credit provision economically unviable regardless of the product innovation applied, or which segments have already been served by earlier FinTech entrants and are therefore significantly more competitive than the headline gap number suggests.

India’s MSME sector has registered over 5 crore businesses on the Udyam portal. These businesses are not a homogeneous credit market. They are a collection of structurally distinct sub-segments with different financial profiles, different documentation capabilities, different cash flow patterns, different collateral availability, and most importantly, different relationships with formal credit that are determined not by trust or technology access but by the underlying economics of serving them.

The FinTech founders who have built sustainable MSME lending businesses in India are not the ones who built the best credit algorithms or the most frictionless digital application experience. They are the ones who correctly identified which specific MSME sub-segment had a credit need that could be served profitably at scale and built their product, their distribution, and their risk model for that sub-segment specifically. The ones who failed and the majority of MSME FinTech products that have launched in India over the last decade have either failed or significantly underperformed their initial projections, and are almost uniformly the ones who built for “the MSME credit gap” as a category, rather than for a specific, researchable, sub-segment within it.

Why the Credit Gap Persists: The Three Structural Reasons That Most Founder Analyses Miss

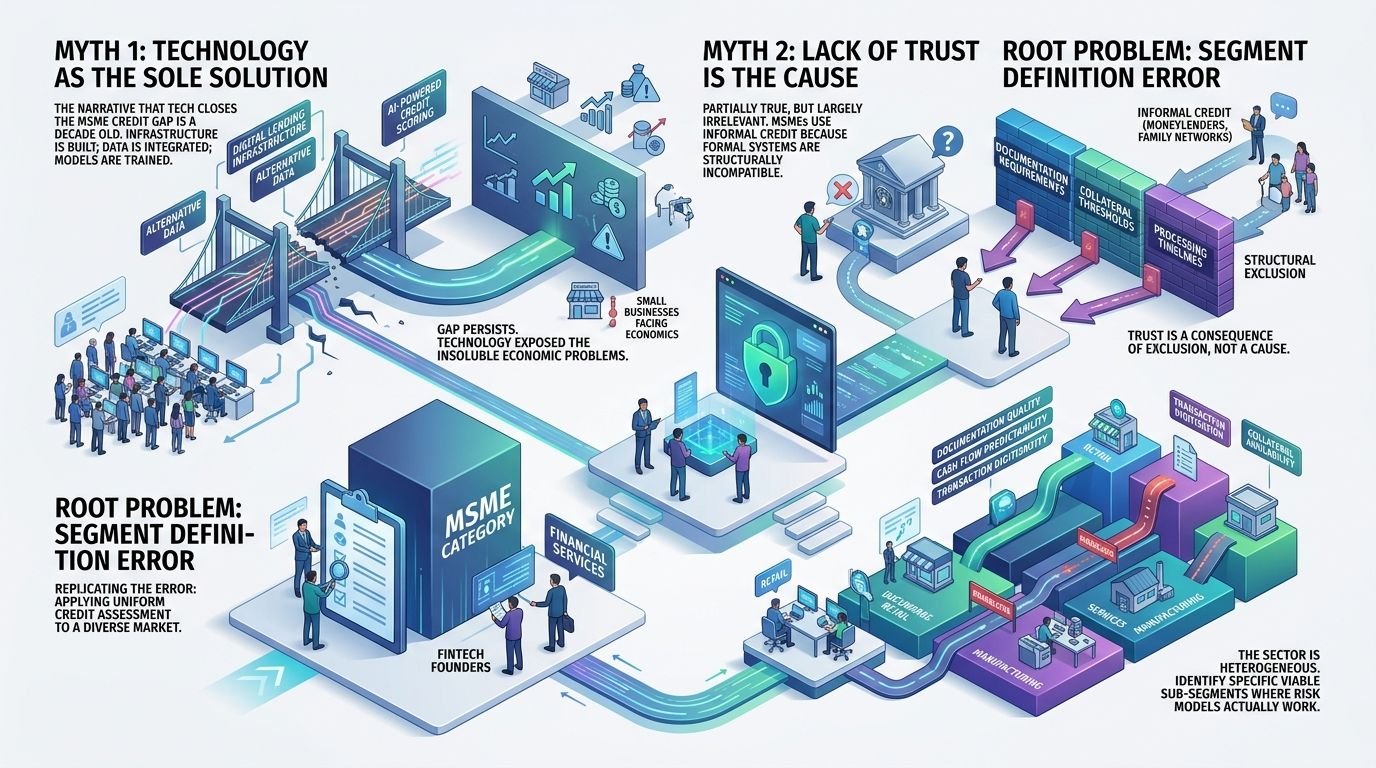

Before identifying the accessible sub-segments, it is worth understanding why the gap exists at all because the answer is not what most FinTech pitch decks claim.

The gap is not primarily a technology problem. The narrative that digital lending infrastructure, alternative data, and AI-powered credit scoring will close the MSME credit gap is a decade old. The infrastructure has been built. The alternative data sources have been integrated. The credit scoring models have been trained. The gap persists at scale because technology solved the parts of the problem that were soluble and exposed the parts that were not, and the insoluble parts are not technology problems. There are economic problems.

The gap is not primarily a trust problem. The narrative that MSME owners distrust formal financial institutions and prefer informal credit is partially true for some sub-segments and largely irrelevant for others. The MSME owners who are currently using informal credit moneylenders, chit funds, and family networks are not doing so because they do not trust banks. Most of them are doing so because the formal credit system’s documentation requirements, collateral thresholds, and processing timelines are structurally incompatible with their business’s financial characteristics. The trust problem is a consequence of structural exclusion, not a cause of it.

The gap is primarily a segment definition problem. The MSME sector contains sub-segments where formal credit provision is economically viable and sub-segments where it is not, and the boundary between those categories is determined by the business’s documentation quality, cash flow predictability, transaction digitisation, and collateral availability. The credit gap persists because the financial services sector has historically applied a uniform credit assessment model to a structurally heterogeneous market, and FinTech founders have largely replicated that error by targeting “MSMEs” as a category rather than the specific sub-segments within it where their product’s risk model actually works.

The 4 MSME Sub-Segments Where FinTech Credit Solutions Have Genuine Product-Market Fit

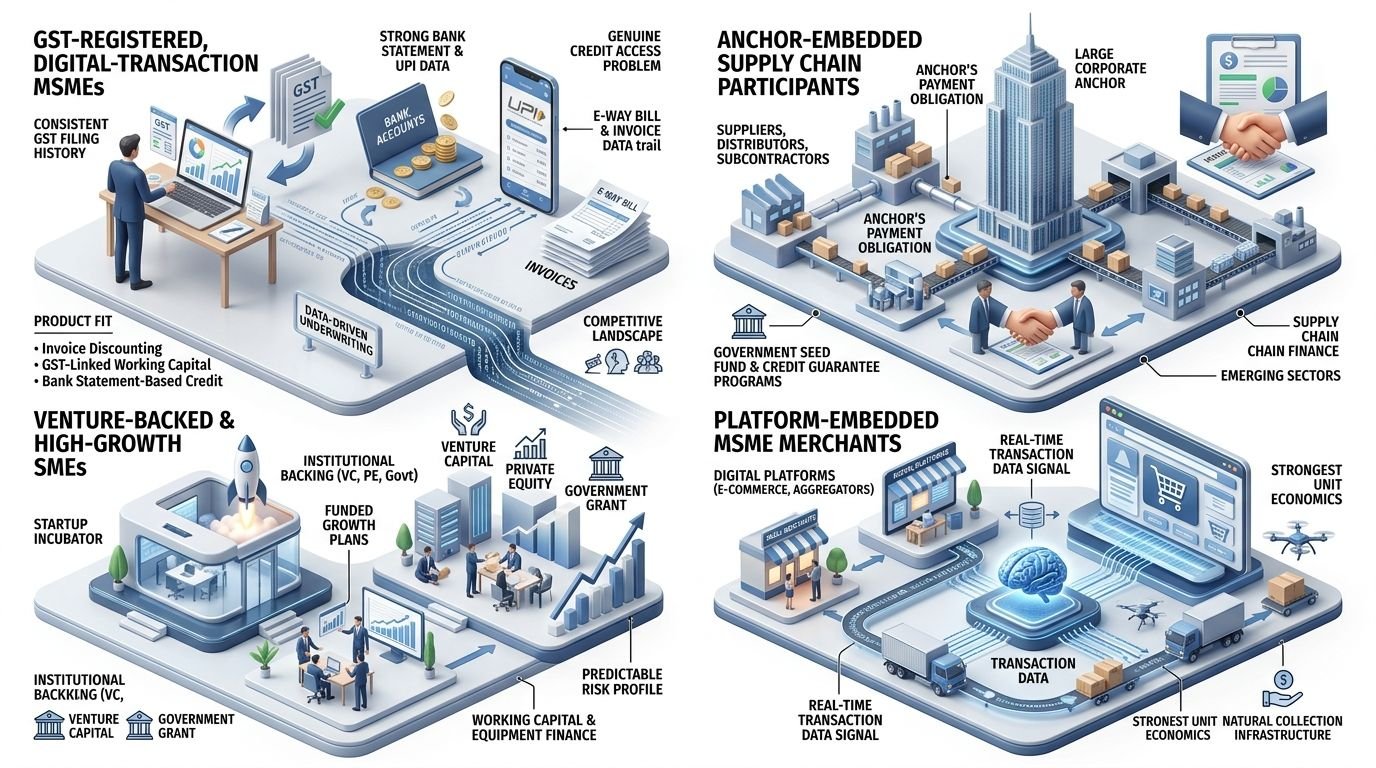

GST-Registered, Digital-Transaction MSMEs

The first and most consistently viable sub-segment for FinTech credit solutions is MSME businesses that file GST regularly, maintain bank accounts with consistent digital transaction history, and operate in sectors where receivables are structured and verifiable. These businesses generate the data trail that alternative credit assessment models require: GST filing history, bank statement patterns, UPI transaction volume, and, in many cases,s e-way bill and invoice data and they face a genuine credit access problem because their balance sheets are too small for traditional bank credit, but their cash flow documentation is sufficient for data-driven underwriting.

The product-market fit in this sub-segment is well-established: invoice discounting, GST-linked working capital, and bank statement-based credit products have demonstrated both demand and recoverable risk profiles in this segment at scale. The competitive density is high — this is the sub-segment that every serious MSME FinTech has prioritised, but the market remains large enough relative to current formal credit penetration that a well-differentiated product with superior distribution can build a sustainable position.

Anchor-Embedded Supply Chain Participants

The second viable sub-segment is MSME businesses that participate in the supply chains of large, creditworthy anchor corporations as suppliers, distributors, or subcontractors, where the anchor’s payment obligation provides the credit risk underpinning that makes the MSME lending decision analytically tractable. Supply chain finance and anchor-embedded lending have produced some of the most defensible unit economics in Indian MSME FinTech because the credit risk is effectively partially transferred to the anchor rather than resting entirely on the MSME’s standalone financial profile.

The accessible opportunity in this sub-segment is directly tied to the expansion of India’s GCC ecosystem and large corporate base, as anchor programs expand, the embedded supply chain credit market expands with them. Government seed-fund and credit-guarantee programs enlarge the potential client universe, especially in fintech, edtech, and software-as-a-service domains, creating additional anchor-like structures that FinTech lenders can leverage.

Venture-Backed and High-Growth SMEs

The third viable sub-segment is startups and SMEs that have institutional backing, venture capital, private equity, or government grant programs, and need working capital or equipment finance to execute against a funded growth plan. These businesses have both the documentation sophistication and the institutional relationship context that make formal credit assessment reliable. The credit need is real, and funded startups consistently face cash flow gaps between equity rounds and the risk profile is more predictable than informal MSME credit because the institutional backer provides a reference point for the business’s viability and trajectory.

Platform-Embedded MSME Merchants

The fourth viable sub-segment is MSME merchants operating within established digital platforms e-commerce sellers, aggregator-platform service providers, and marketplace vendors where the platform’s transaction data provides a credit assessment signal of unusual reliability. Platform-embedded lending, pioneered by the large e-commerce platforms, has demonstrated the strongest unit economics in MSME FinTech because the transaction data is real-time, the platform relationship creates a natural collection infrastructure, and the merchant’s business dependency on the platform creates repayment motivation that standalone lending relationships cannot replicate.

The 3 MSME Sub-Segments Where FinTech Credit Solutions Consistently Fail

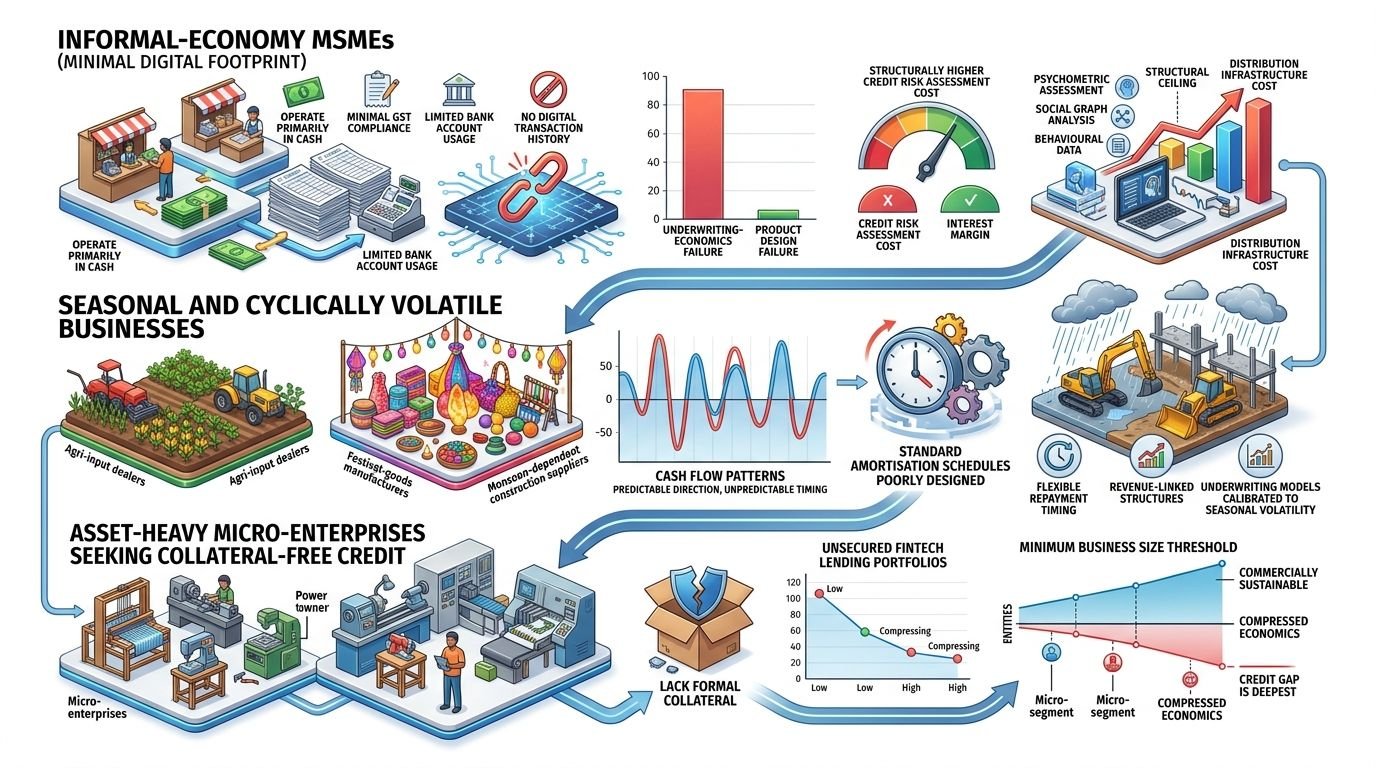

Informal-Economy MSMEs With Minimal Digital Footprint

The largest sub-segment of India’s registered MSME population, businesses operating primarily in cash, with minimal GST compliance, limited bank account usage, and no digital transaction history, is the sub-segment that most FinTech founders cite as their addressable market and most consistently fail to serve sustainably. The failure is not a product design failure. It is an underwriting-economics failure: the cost of credit risk assessment for businesses without a verifiable data trail is structurally higher than the interest margin available for the loan sizes these businesses require.

Every FinTech solution that has claimed to solve informal-economy MSME credit using psychometric assessment, social graph analysis, or behavioural data has encountered the same structural ceiling. At the loan sizes and tenors that informal-economy MSMEs need, the risk-adjusted returns do not support the underwriting cost unless the portfolio is so large and so diversified that it requires the kind of distribution infrastructure that eliminates the unit economics advantage the FinTech claimed over traditional banks.

Seasonal and Cyclically Volatile Businesses

MSMEs with highly seasonal revenue patterns, such as agricultural input dealers, festival-goods manufacturers, and monsoon-dependent construction suppliers, face a credit gap that is real but structurally resistant to standard FinTech lending models. The cash flow patterns of these businesses are predictable in direction but unpredictable in timing, creating repayment risk profiles that standard amortisation schedules are poorly designed to accommodate. The credit products these businesses actually need are structurally different from standard working capital; they require flexible repayment timing, revenue-linked structures, and underwriting models calibrated to seasonal volatility rather than monthly cash flow consistency.

Asset-Heavy Micro-Enterprises Seeking Collateral-Free Credit

Micro-enterprises, the smallest tier of India’s MSME population, that require credit for physical asset acquisition but lack formal collateral, consistently produce recovery rates in unsecured FinTech lending portfolios that compress the economics below viability. The collateral-free credit promise that most MSME FinTech products make is commercially sustainable only above a minimum business size threshold that excludes the micro-enterprise segment, where the credit gap is actually deepest.

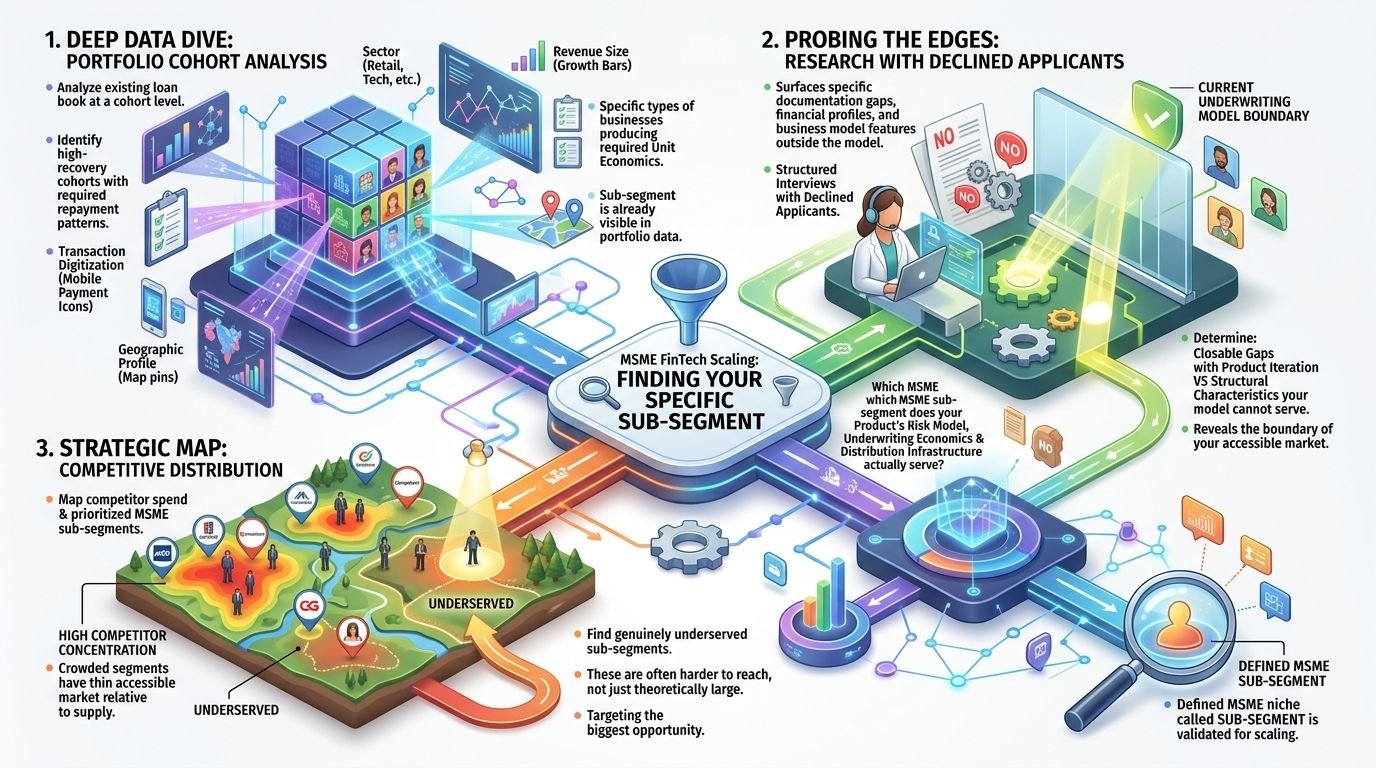

The Primary Research Methodology for Identifying Your Actual Sub-Segment

The research question every MSME FinTech founder needs to answer before scaling acquisition spend is not “how large is the MSME credit gap?” It is “which specific sub-segment of the MSME market does my product’s risk model, underwriting economics, and distribution infrastructure actually serve and is that sub-segment large enough and accessible enough to support the business I am trying to build?”

Answering that question requires three specific research exercises.

The first is a portfolio cohort analysis of your existing loan book, if you have one. Not aggregate portfolio performance, but cohort-level analysis: which specific types of businesses, defined by sector, revenue size, documentation quality, transaction digitisation, and geographic profile, are producing the recovery rates and repayment patterns your unit economics require? The sub-segment your product actually works for is already visible in your portfolio data if you are willing to look at it with segment-level specificity rather than aggregate metrics.

The second is primary research with declined applicants, the MSME businesses that applied for credit through your platform and were declined. These businesses reveal, more clearly than any accepted applicant cohort, the boundary of your current underwriting model’s accessible market. Structured interviews with declined applicants consistently surface the specific documentation gaps, financial profile characteristics, and business model features that sit outside your current risk model of those gaps are closable with product iteration, versus which represent structural characteristics of sub-segments your model cannot serve.

The third is competitive distribution analysis mapping where your direct competitors are concentrating their acquisition spend and which MSME sub-segments they are prioritising. In a market as crowded as MSME lending, the sub-segments with the highest competitor concentration are not necessarily the largest opportunity; they are the segments that have been most thoroughly tested and where the accessible market relative to the competitive supply is thinnest. The accessible opportunity is more often found in the sub-segments that are genuinely underserved because they are harder to reach, not in the sub-segments that are theoretically large but already crowded.

What To Do Next — Monday Morning Actions

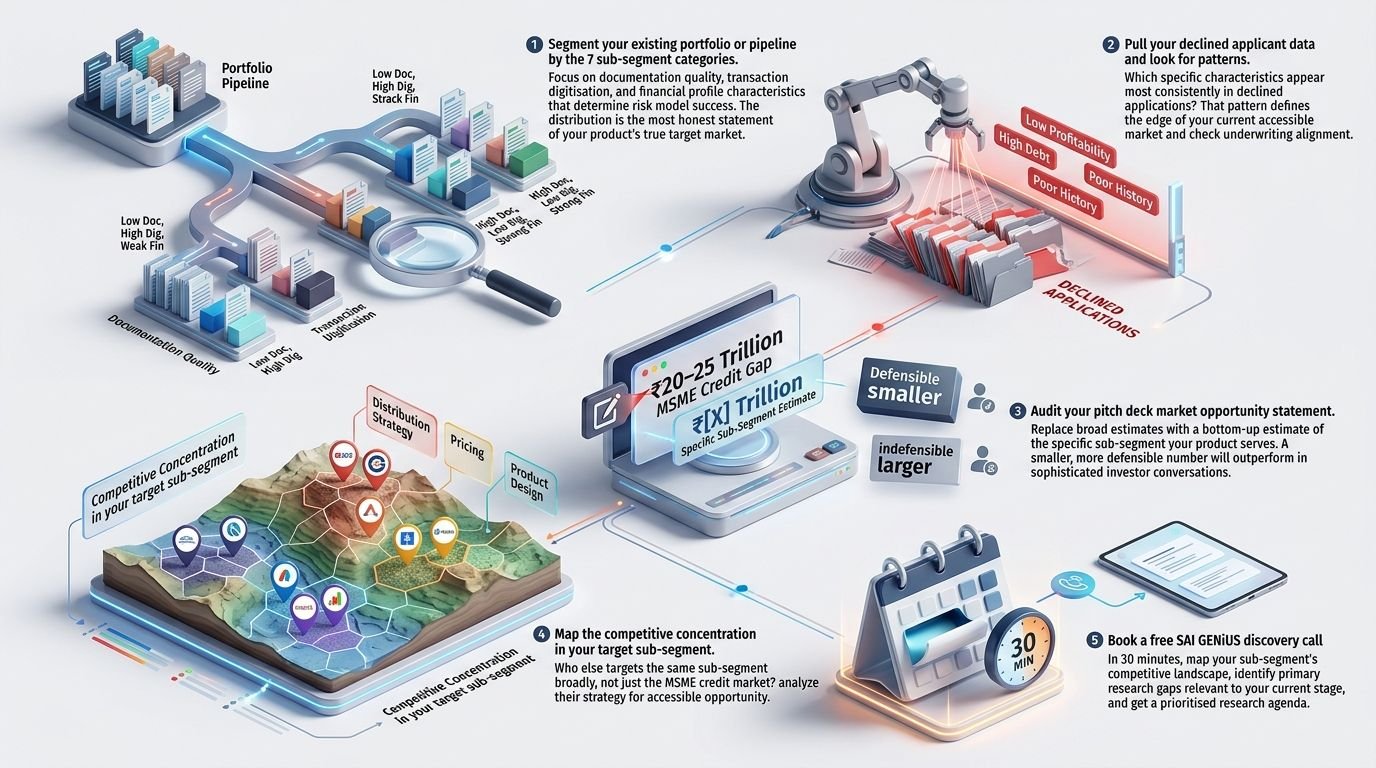

1. Segment your existing portfolio or pipeline by the 7 sub-segment categories in this article. Not by sector or loan size by the documentation quality, transaction digitisation, and financial profile characteristics that determine whether your risk model actually works for that business. The distribution of your portfolio across those categories is the most honest statement of your product’s true target market.

2. Pull your declined applicant data and look for patterns. Which specific characteristics appear most consistently in declined applications? That pattern defines the edge of your current accessible market and tells you whether the sub-segment you are targeting in your acquisition strategy is actually the sub-segment your underwriting model serves.

3. Audit your pitch deck market opportunity statement. If it says “₹20–25 trillion MSME credit gap” without sub-segment specificity, replace it with a bottom-up estimate of the specific sub-segment your product serves. A smaller, more defensible number will consistently outperform a larger, indefensible one in a sophisticated investor conversation.

4. Map the competitive concentration in your target sub-segment. Who else is specifically targeting the same sub-segment, not just the MSME credit market broadly and what does their distribution strategy, pricing, and product design tell you about the accessible opportunity within it?

5. Book a free SAI GENiUS discovery call. In 30 minutes, we will map your specific sub-segment’s competitive landscape, identify the primary research gaps most relevant to your current stage, and give you a prioritised research agenda before the call ends.

Related Posts

Crores of Indian MSMEs. Most Without Professional Research. Here Is Exactly What They Are Missing and What It Is Costing Them.

India's MSME sector is the backbone of the national economy by almost any metric you…