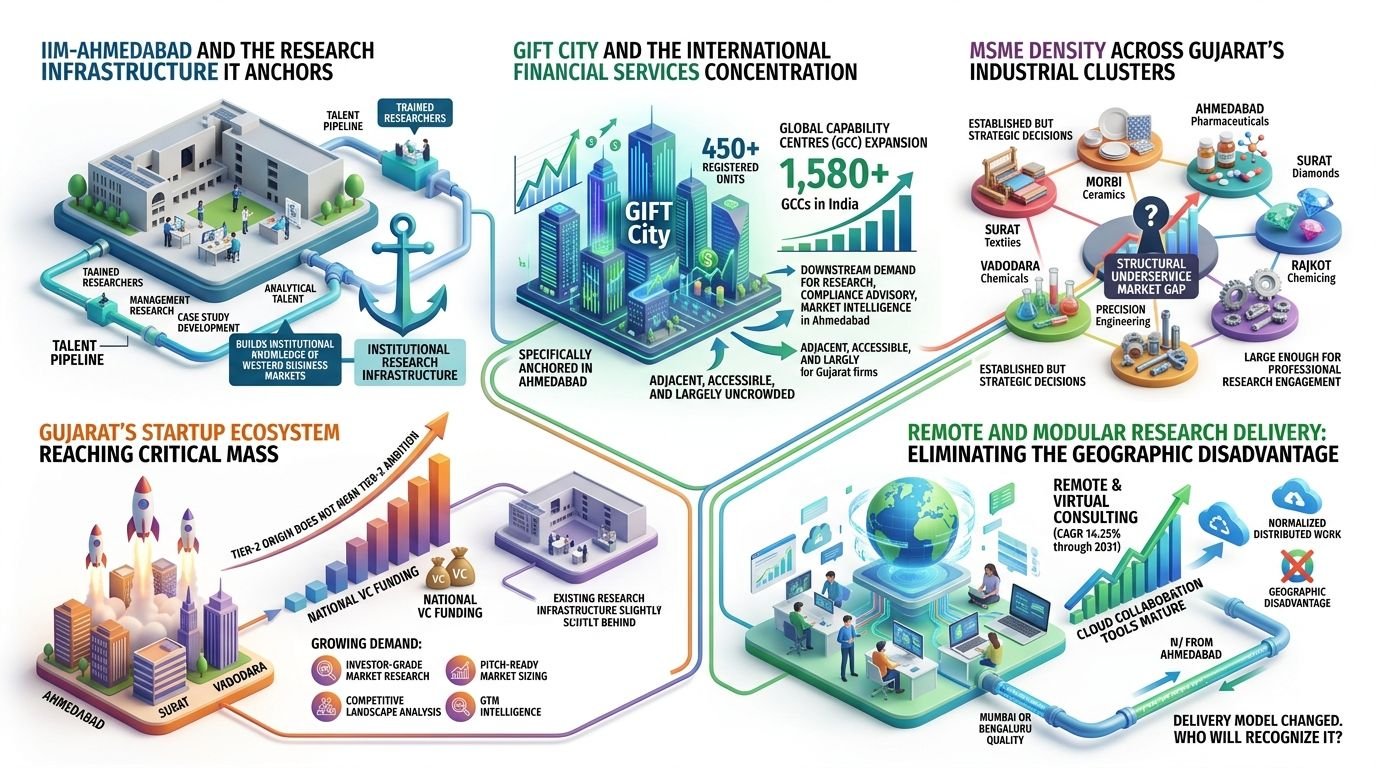

IIM-Ahmedabad and the Research Infrastructure It Anchors

IIM-Ahmedabad is one of Asia’s premier management institutions and its presence in Ahmedabad creates an institutional research infrastructure that most Indian cities outside the traditional metro cluster do not have. The concentration of management research, case study development, and analytical talent that IIM-A produces and attracts is not simply an academic asset. It is the foundation of a professional intelligence ecosystem producing trained researchers, building institutional knowledge of India’s western business markets, and creating the talent pipeline that intelligence-focused firms operating in Ahmedabad can access.

GIFT City and the International Financial Services Concentration

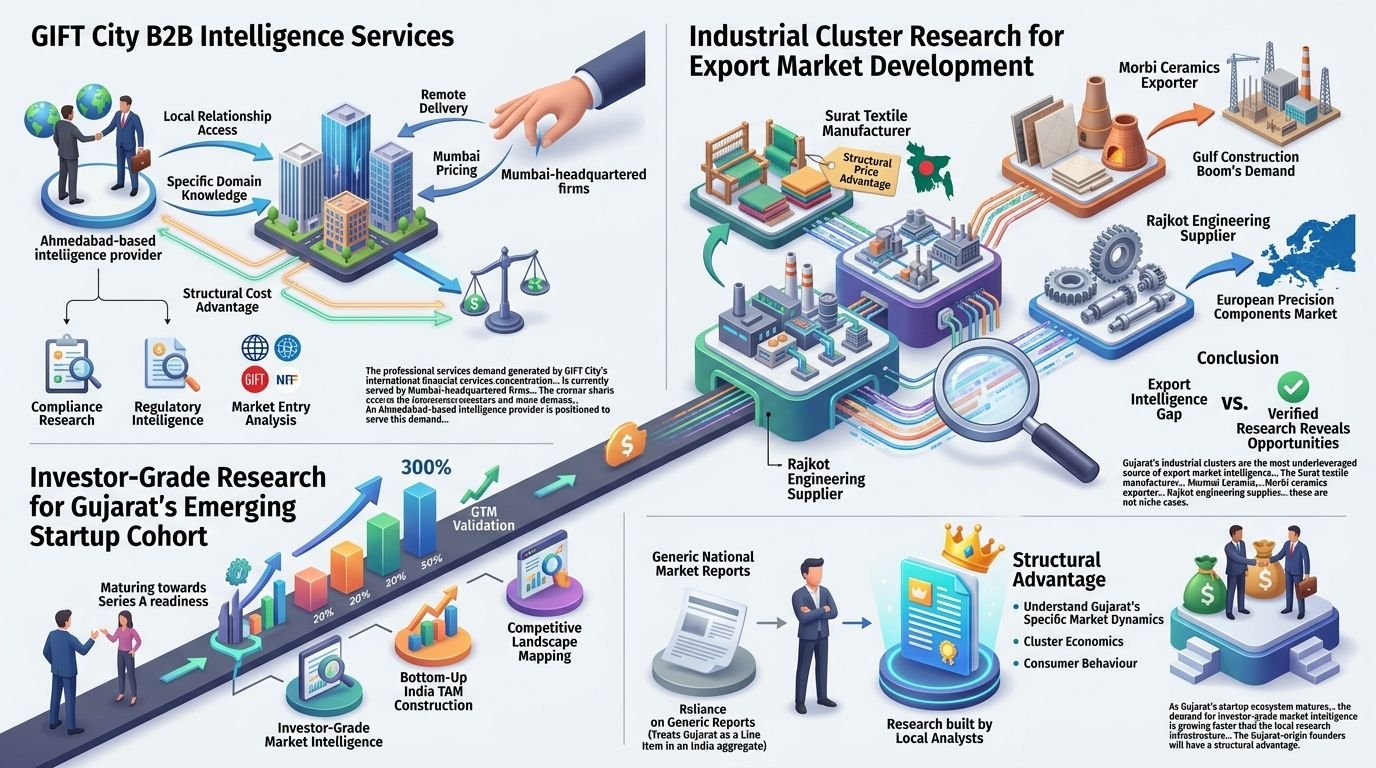

GIFT City’s 450+ registered units represent a concentration of international financial services activity that has no precedent outside Mumbai in the Indian context. More than 1,580 global capability centres already operate in India, and the GCC expansion dynamic, combined with GIFT City’s international financial services infrastructure, is creating a downstream demand for professional research, compliance advisory, and market intelligence that is specifically anchored in the Ahmedabad geography. For Gujarat-based intelligence firms and professional services businesses, this demand is adjacent, accessible, and largely uncrowded.

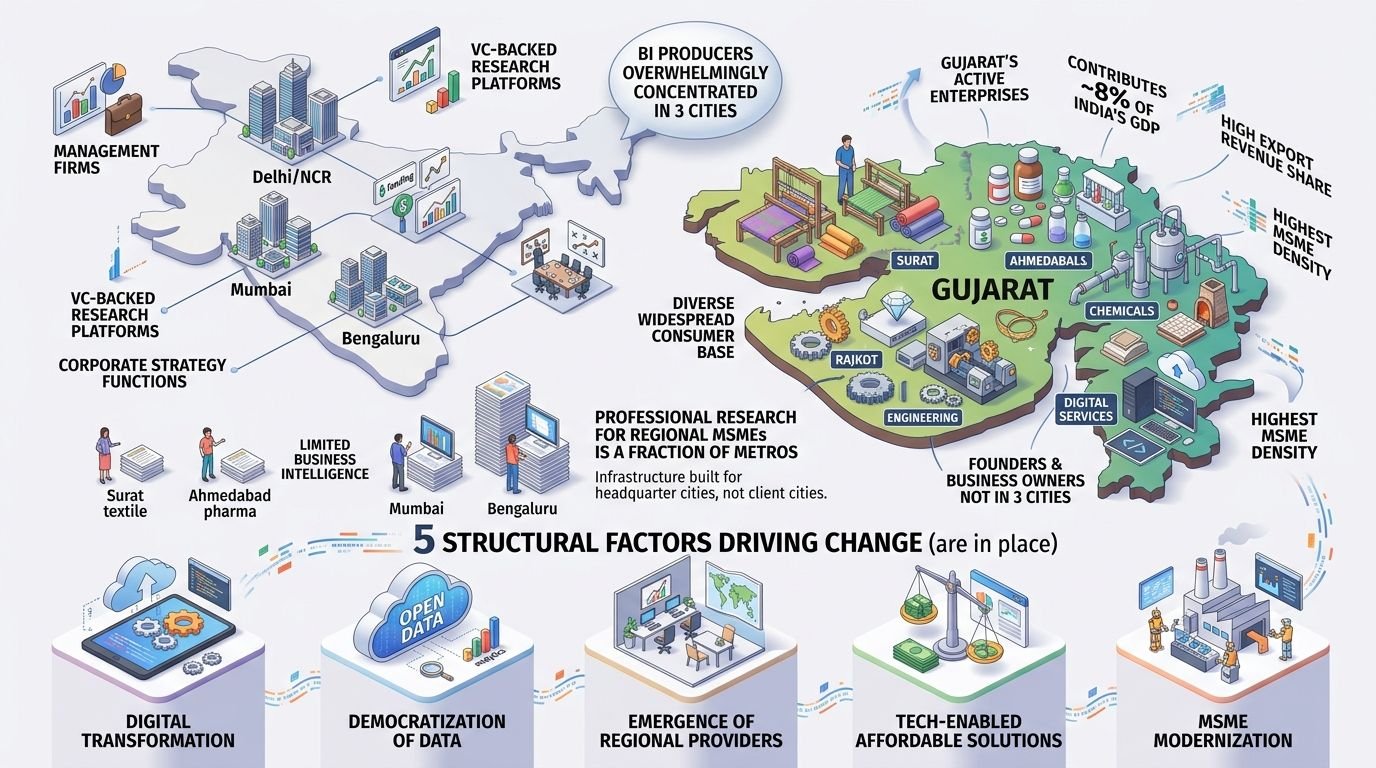

MSME Density Across Gujarat’s Industrial Clusters

Gujarat’s industrial clusters textiles in Surat, ceramics in Morbi, pharmaceuticals in Ahmedabad, diamonds in Surat, chemicals in Vadodara, precision engineering in Rajkot represent extraordinary concentrations of businesses at a common stage of development: established enough to have real strategic decisions to make, growing fast enough that the cost of making the wrong ones is significant, and large enough that a scoped professional research engagement is financially accessible. The structural underservice of this cluster by institutional research is not a permanent condition. It is a market gap, and market gaps in growing sectors close.

Gujarat’s Startup Ecosystem Reaching Critical Mass

Gujarat’s startup ecosystem, anchored in Ahmedabad, Surat, and Vadodara, has historically been underrepresented in national VC funding flows relative to its economic size. That underrepresentation is beginning to close as a cohort of Gujarat-origin startups demonstrates that Tier-2 origin does not mean Tier-2 ambition. As Gujarat’s startup ecosystem reaches the scale at which institutional investor attention follows, the demand for investor-grade market research, pitch-ready market sizing, competitive landscape analysis, and GTM intelligence is growing at a rate that the existing research infrastructure in the city is not yet meeting.

Remote and Modular Research Delivery: Eliminating the Geographic Disadvantage

Remote and Virtual Consulting is set to climb at a 14.25% CAGR through 2031 as cloud collaboration tools mature and clients normalise distributed work. This structural shift in consulting delivery is the single most important development for Gujarat business owners in the intelligence market because it eliminates the geographic rationale for the intelligence gap. A research engagement that previously required proximity to a Mumbai or Bengaluru consulting office can now be delivered with identical quality from and to Ahmedabad. The delivery model has changed. The question is which Gujarat businesses will be the first to recognise it.