India’s MSME sector is the backbone of the national economy by almost any metric you choose to apply. It contributes approximately 30% of GDP, accounts for roughly 45% of total exports, and employs well over 10 crore people. By sheer economic weight, it is one of the most consequential sectors in the country.

It is also the most underserved by professional market intelligence of any major business segment in India — and the gap between the intelligence available to a well-resourced corporate and the intelligence available to a typical Indian MSME owner is not closing. Until recently, it was widening.

The reason is structural and entirely logical. Institutional market research — the kind that produces verified, sector-specific, strategically actionable intelligence — has historically been priced for institutional buyers. A comprehensive market research engagement from a reputable firm costs ₹5–25 lakhs. A syndicated research report from an international database costs ₹1–5 lakhs for a single download. Neither figure is accessible to a business running at ₹3–10 crore annual revenue with a working capital cycle that leaves no discretionary budget for intelligence that does not have an immediate, visible operational application.

So MSME owners do what rational people do when institutional resources are inaccessible. They rely on what they have: decades of industry experience, networks of peers and suppliers, gut instinct refined over years of operation, and the accumulated pattern recognition that comes from running a business in one sector for a long time.

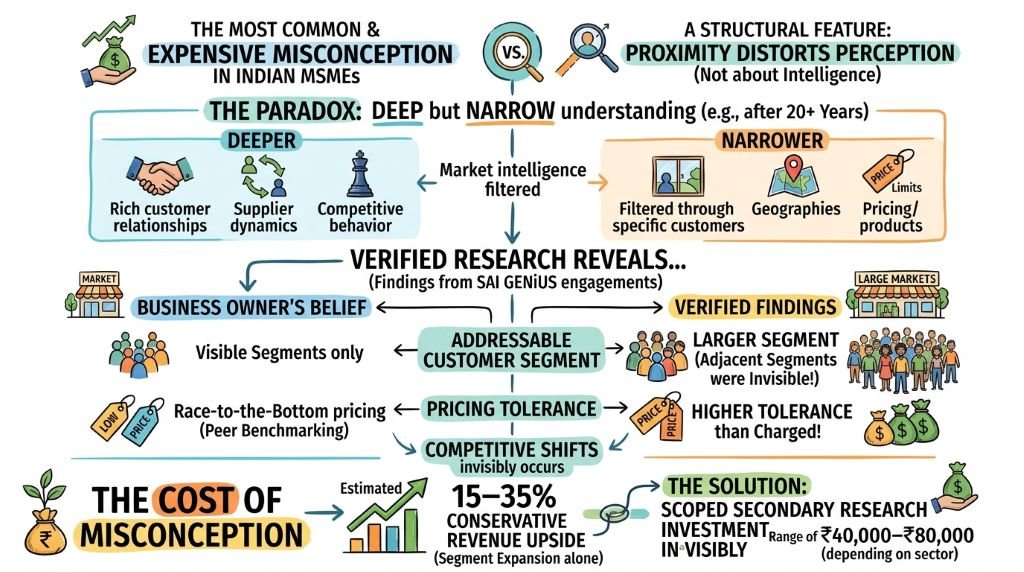

These are genuinely valuable inputs. They are also, in isolation, structurally insufficient — and the gap between what they produce and what verified research produces is not theoretical. It has a cost. In every case. In every sector. At every scale.

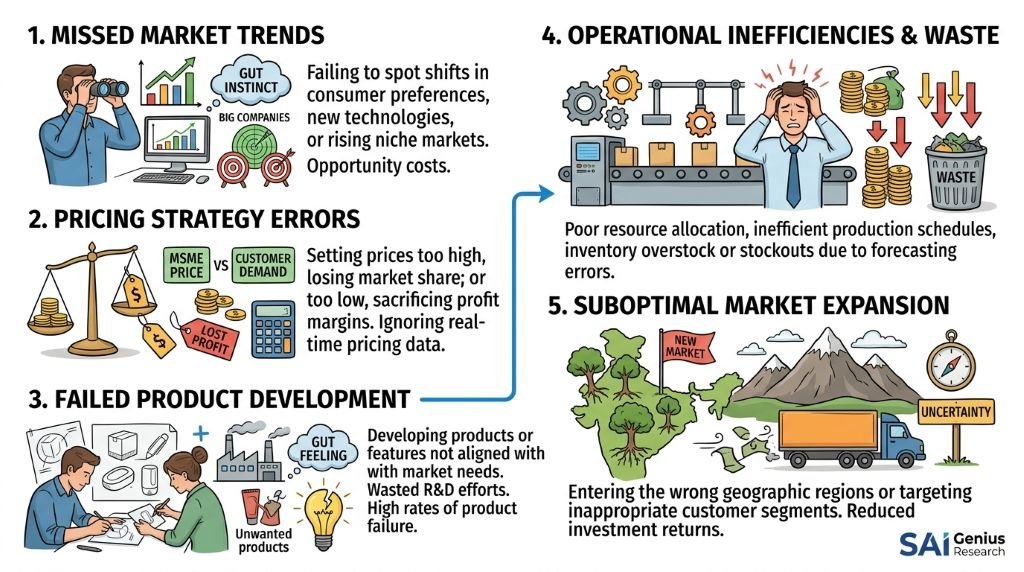

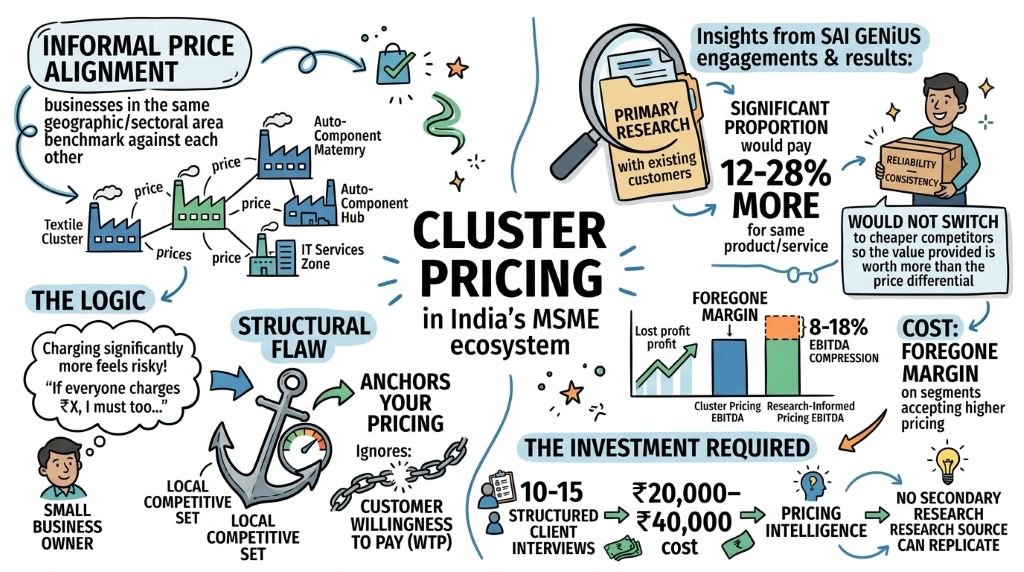

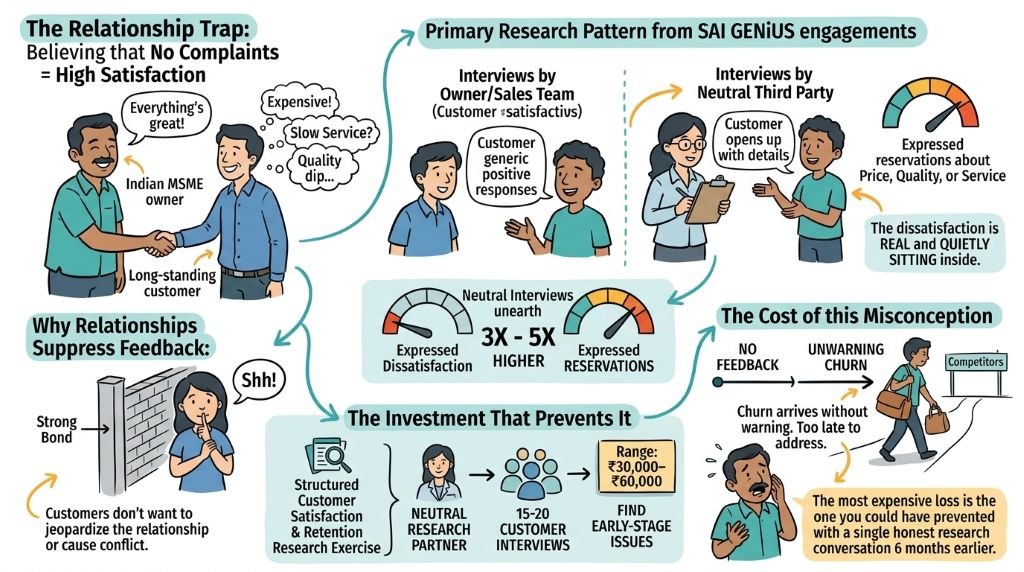

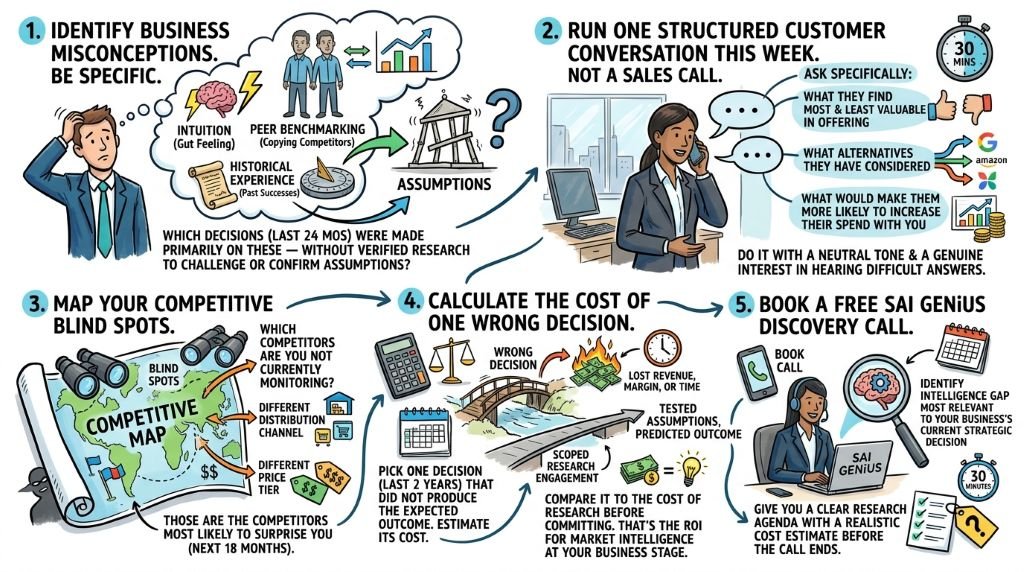

Here are the 5 places where SAI GENiUS research has most consistently found that cost.