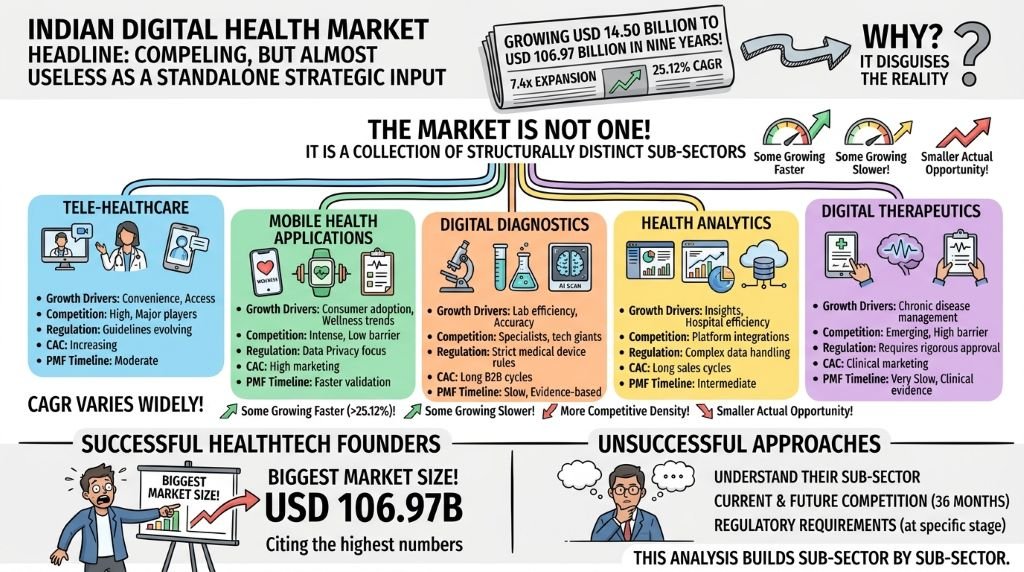

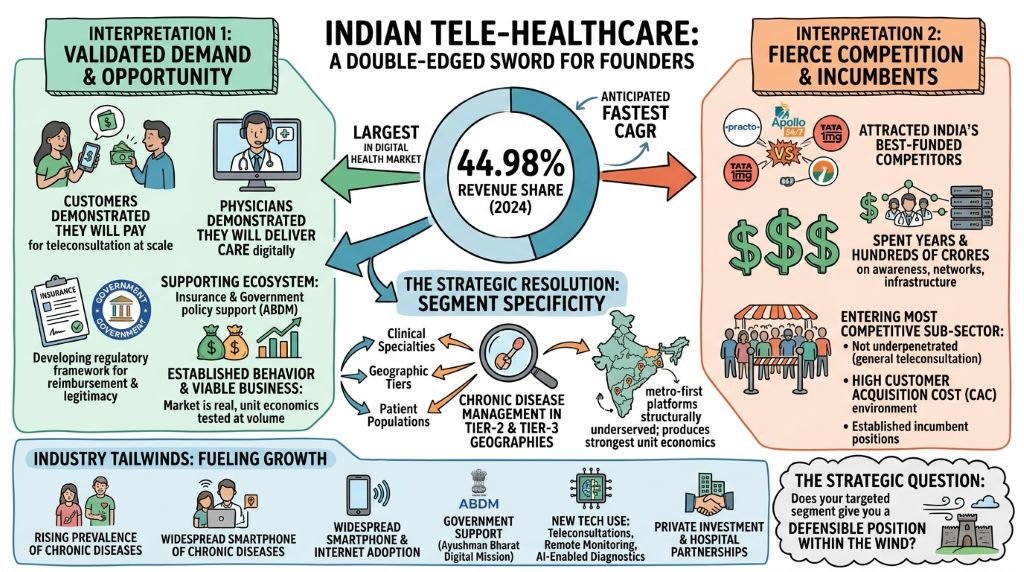

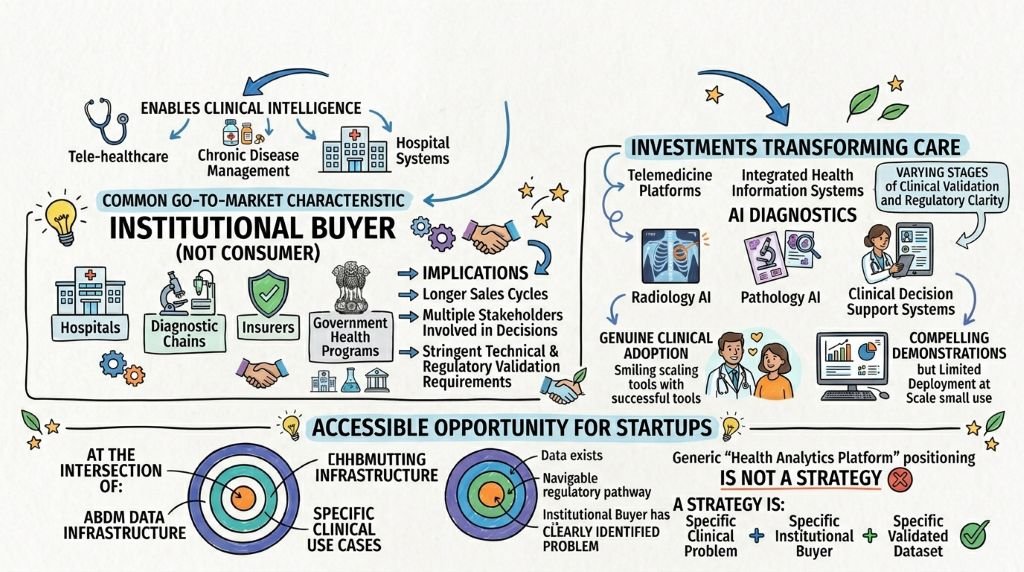

The tele-healthcare segment dominated the Indian digital health market with the largest revenue share of 44.98% in 2024 and is anticipated to grow at the fastest CAGR over the forecast period.

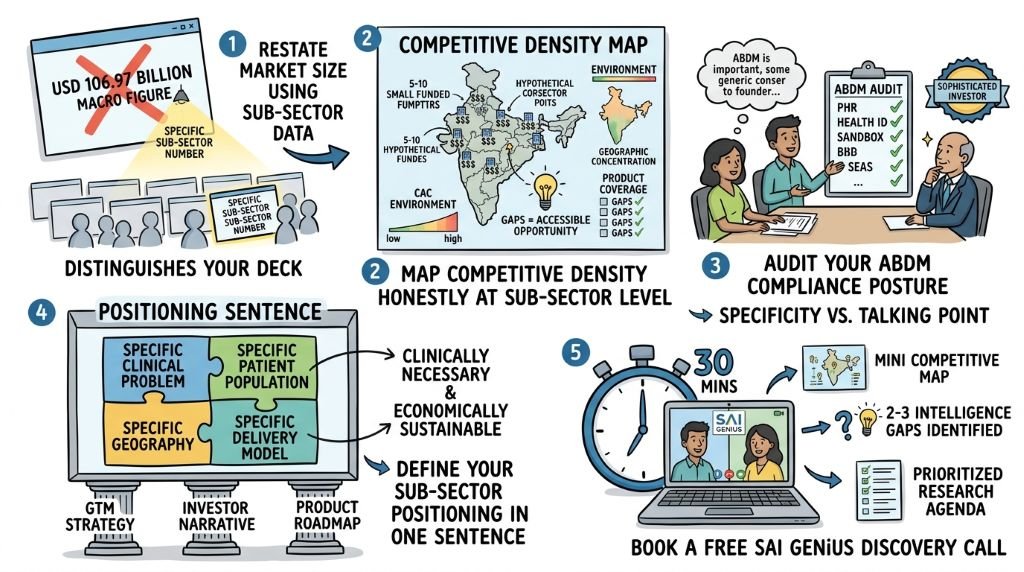

Nearly half of India’s entire digital health market revenue is concentrated in one sub-sector. For a HealthTech founder, that number requires two simultaneous and opposite interpretations.

The first interpretation is that tele-healthcare is where the validated demand is. Customers have demonstrated, at scale, that they will pay for teleconsultation services. Physicians have demonstrated that they will deliver care through digital platforms. Insurance companies and government payers have demonstrated, through ABDM integration and policy support, that the regulatory framework for reimbursement and legitimacy is developing. The market is real, the behavior is established, and the unit economics at the leading platforms have been tested at significant volume.

The second interpretation is that 44.98% revenue share, growing at the fastest CAGR in the sector, with government tailwind and established consumer behavior, is a description of a market that has already attracted India’s best-funded competitors. Practo, Apollo 24/7, Tata 1mg, and a cohort of well-capitalized challengers have spent years and hundreds of crores building consumer awareness, physician networks, and technology infrastructure in this sub-sector. A new entrant in general teleconsultation is not entering an underpenetrated market. They are entering the most competitive sub-sector in Indian digital health with the highest CAC environment and the most established incumbent positions.

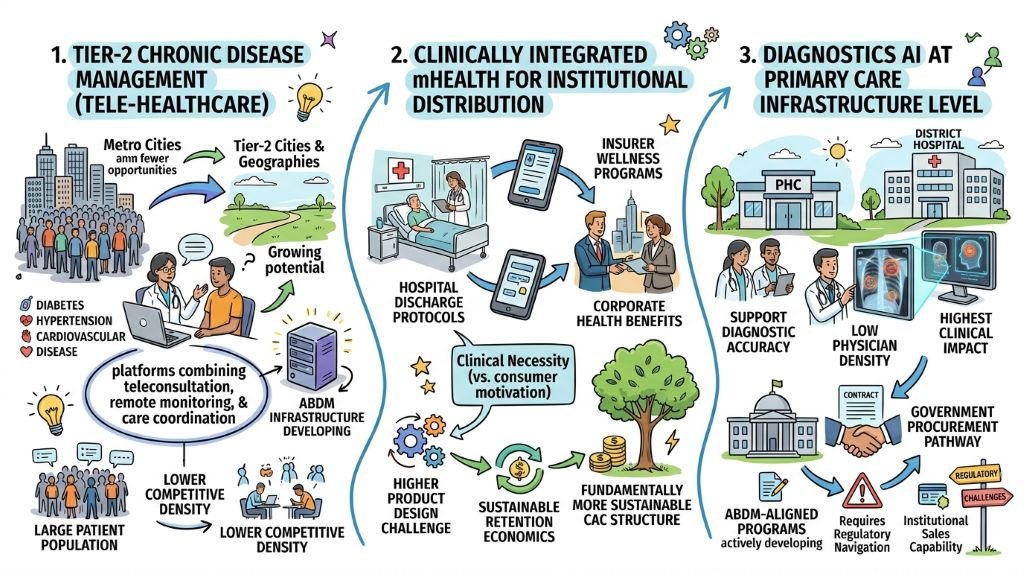

The strategic resolution is segment specificity within tele-healthcare — not the general teleconsultation market, but specific clinical specialties, specific geographic tiers, or specific patient populations where the incumbent platforms have structural limitations. The largest of those opportunities, validated by the data, is chronic disease management in Tier-2 and Tier-3 geographies — a segment that the metro-first platforms are structurally underserving and that produces the strongest unit economics in the sub-sector.

Growth in tele-healthcare is driven by rising chronic disease prevalence, widespread smartphone and internet adoption, and government support through the Ayushman Bharat Digital Mission. Increasing use of teleconsultations, remote monitoring, and AI-enabled diagnostics, along with private sector investments and hospital partnerships, is accelerating adoption. These are the tailwinds. The strategic question for a new entrant is not whether the tailwinds are real — they are — but whether the specific segment they are targeting gives them a defensible position within the wind.